ON-255: NFT Marketplaces 🤝

Coverage on OpenSea, Blur, Rarible and Hyperspace

Jul 26, 2024

Distributed research for distributed networks — OurNetwork is crypto's go-to platform for onchain analytics.OpenSea, Blur, Rarible, Hyperspace

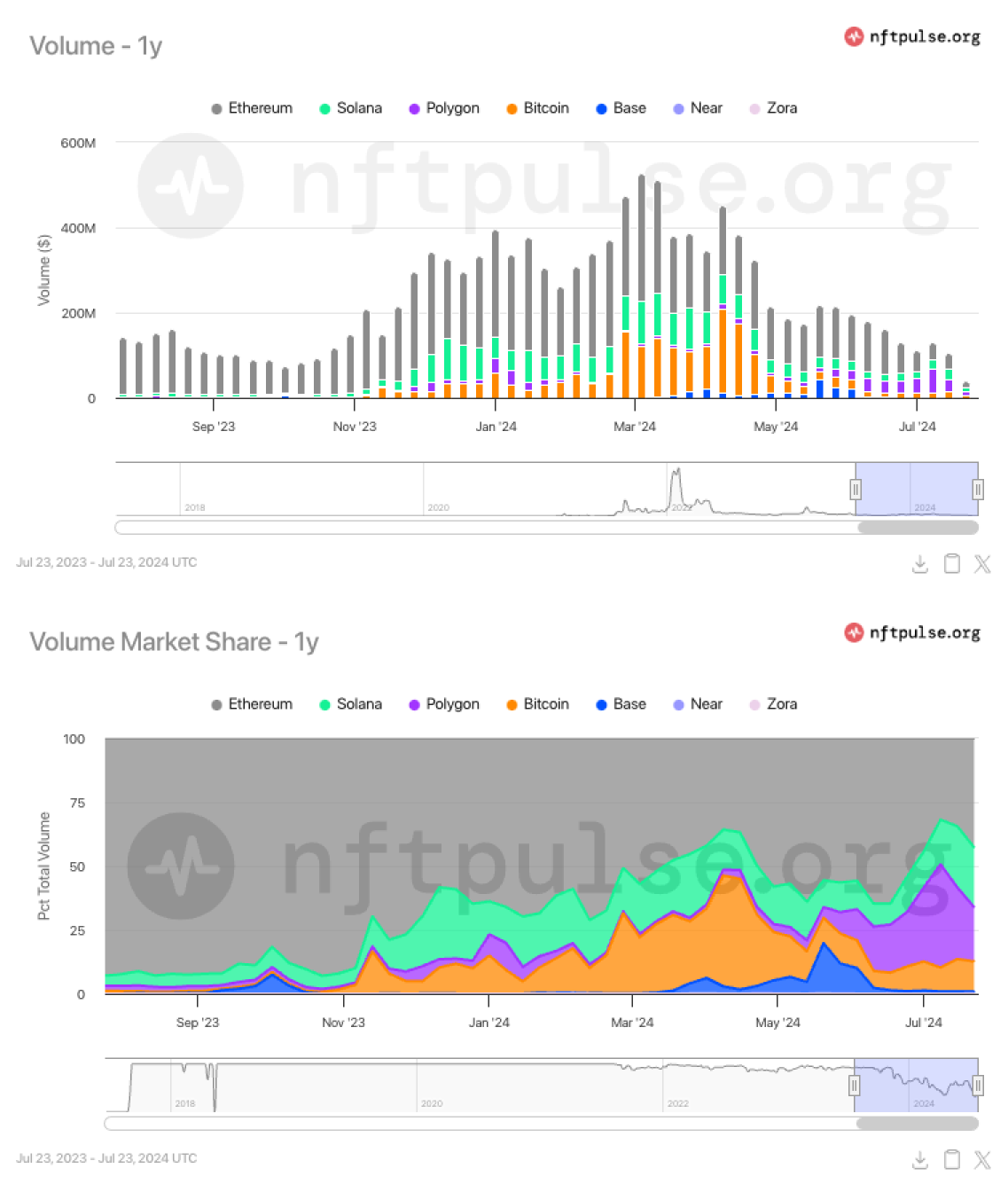

- NFT trading volume dropped by 50% since April 2024 from $300M/week to less than $150M/week. Over the past 30 days, daily trading volume held steady at around $15M. As of July 24, Ethereum has the biggest share of trading volume at $5.8M daily (45% of market share), followed by Solana at $3.3M (26%) and Polygon at $2.3M (18%).

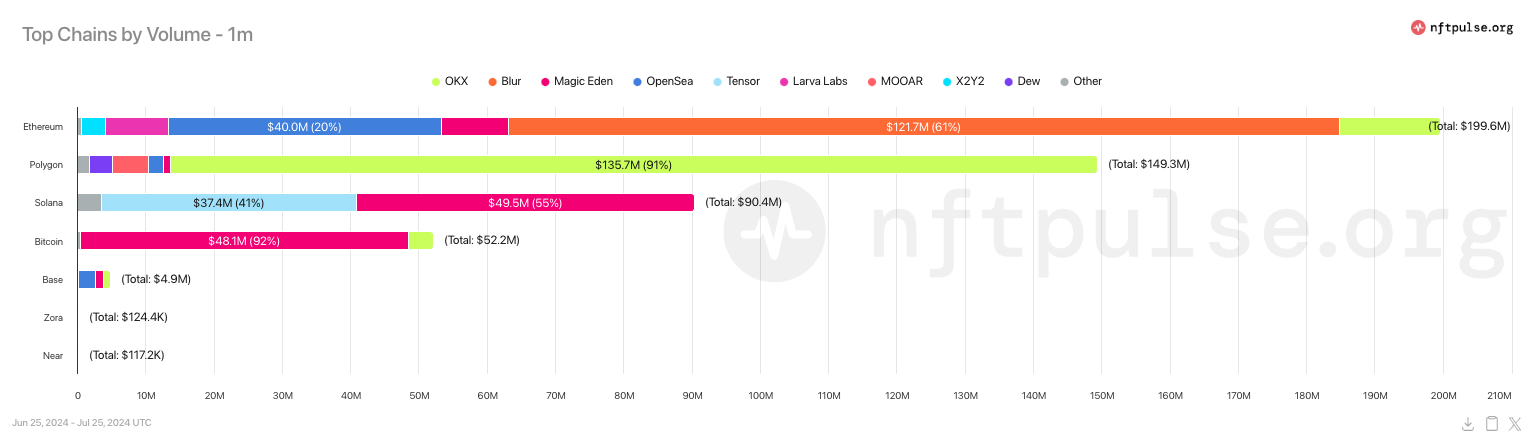

- 1 or 2 platforms dominate trading on each chain. Over the past 30 days on Ethereum, Blur lead with 60% of trading volume. On Polygon, OKX facilitated 91% of trades. On Solana, majority of the volume is from Magic Eden (55%), followed by Tensor (41%). For Bitcoin, Magic Eden hosted over 90% of trades.

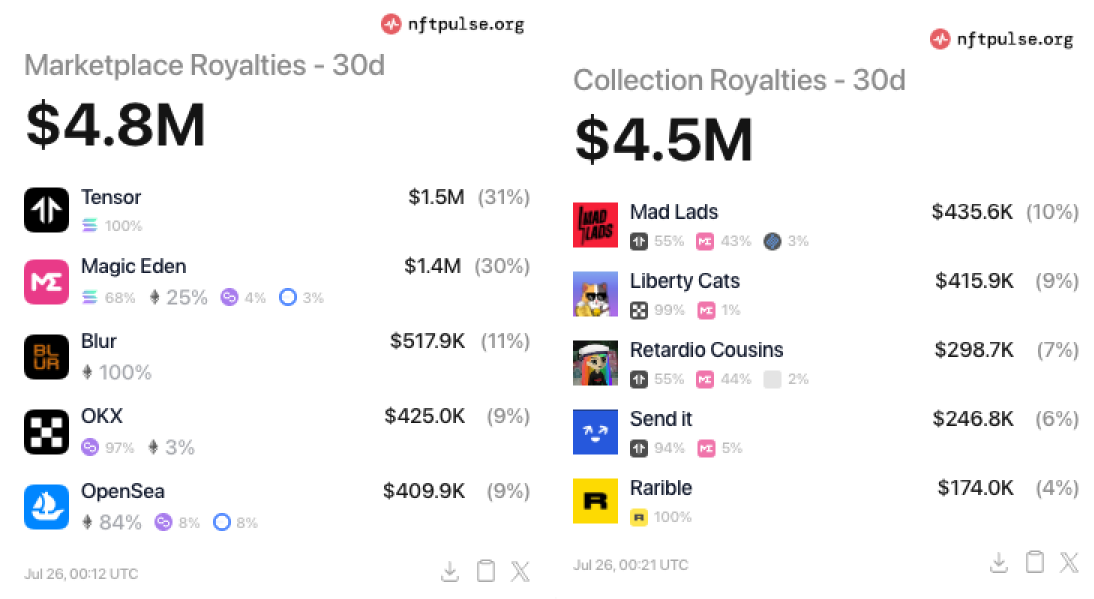

- Royalties continue to be strong, with Solana leading. Over the last 30 days, platforms paid creators $4.8M in royalties. Tensor accounted for 31% and Magic Eden for 30% of these payments. The top collections by royalties were Mad Lads and Liberty Cats, each contributing about 10% of the total.

👥 Evgeni Averkin | Website | Dashboard

📈 Whale Games: Blur's 40-70% volume dominance hinges on 5-20% of traders, leading to a 38% TVL nosedive as incentives dry up

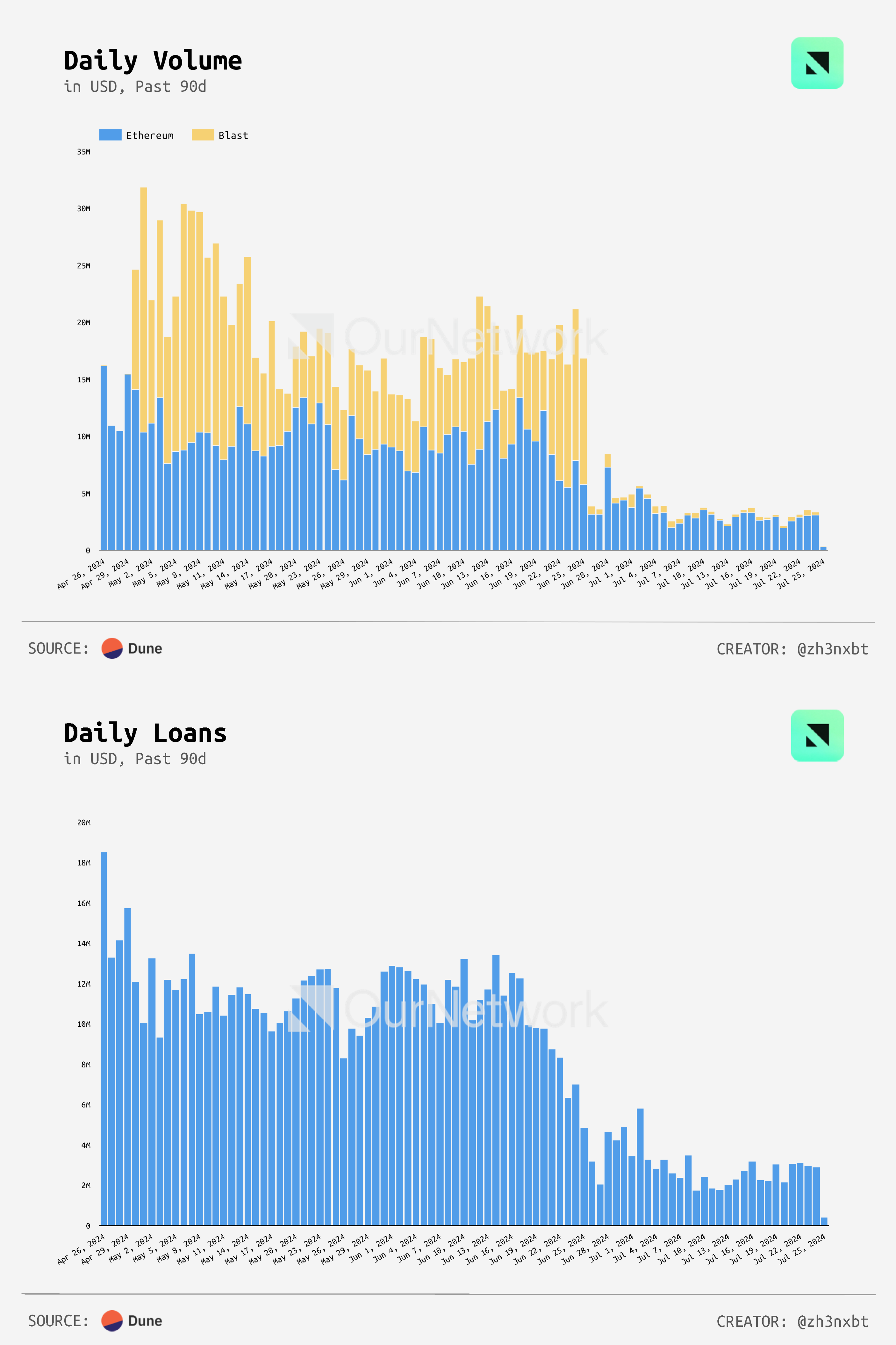

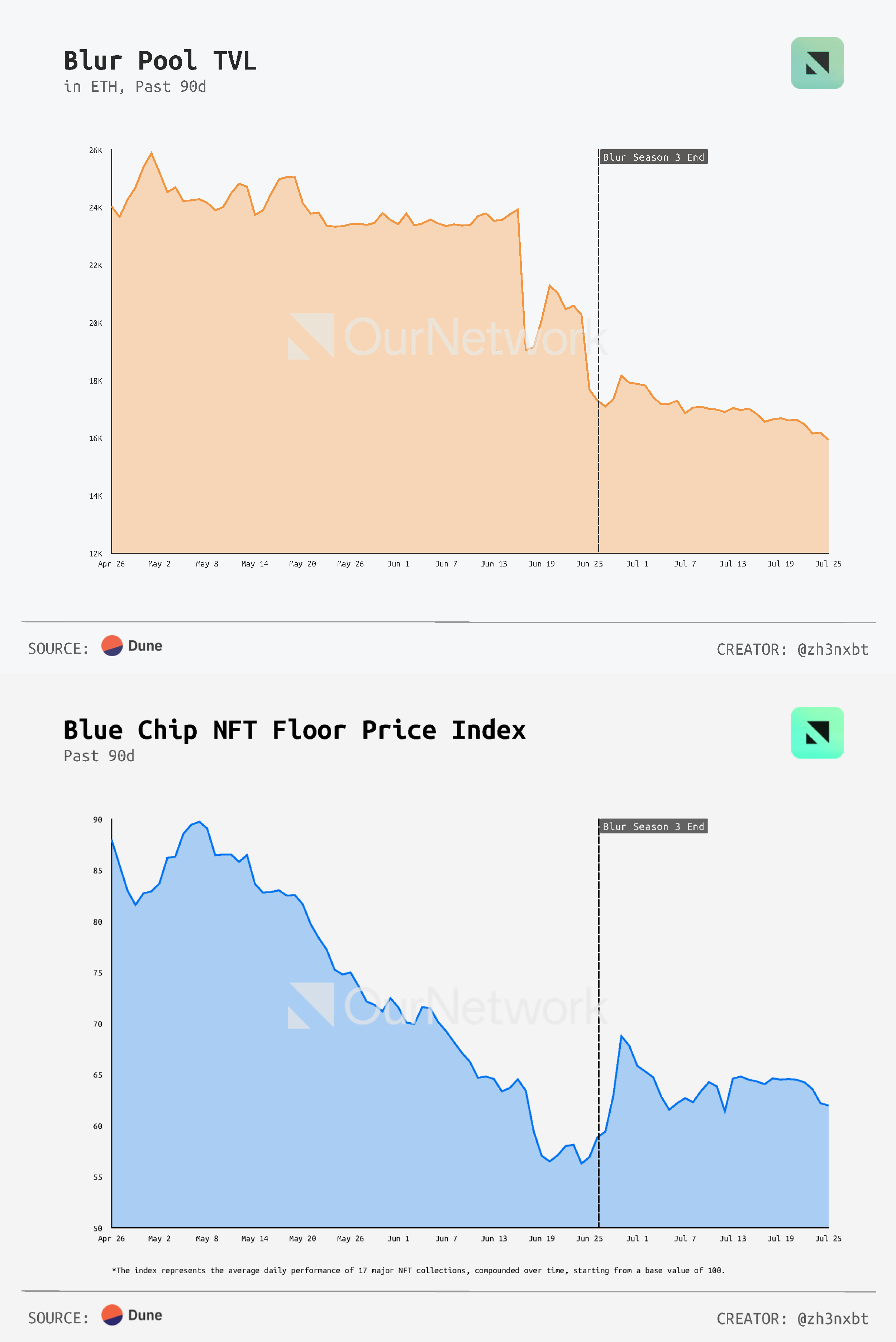

- Blur, a leading NFT marketplace, saw a significant downturn after its Season 3 rewards on Blast ended on June 26. Daily volumes plummeted from $13.3M (Blast) and $7.9M (Ethereum) on June 24 to just $755K and $3.1M, respectively, by June 26. Lending also crashed from $7M to $3.2M. Despite the rewards being exclusive to Blast, farmers exiting one blockchain had spillover effects on another within the same platform, highlighting the volatile nature of incentive-driven crypto ecosystems.

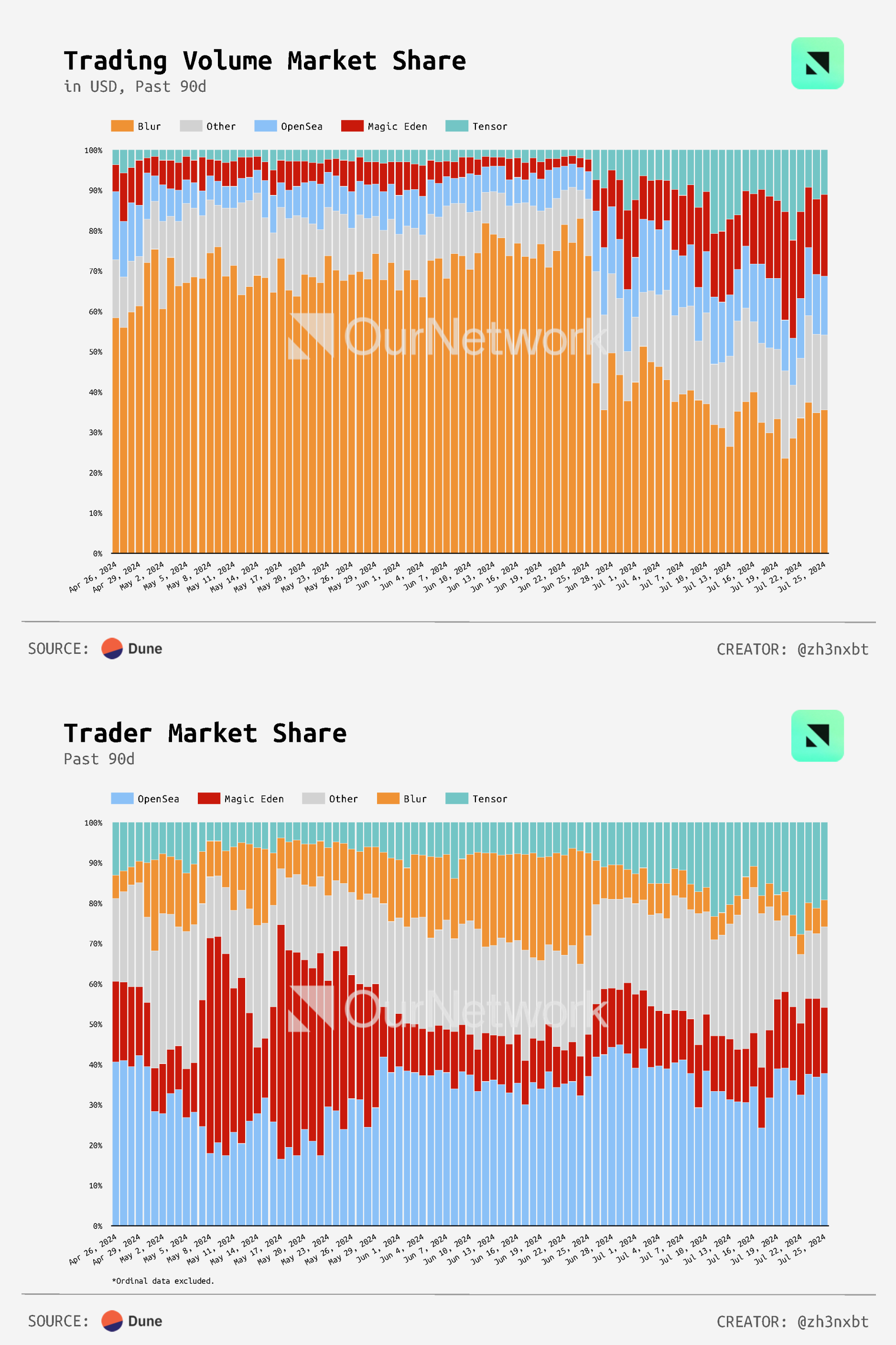

- Blur's volume dominance masks its small trader base. While commanding 40-70% of trading volume from May-July 2024, it consistently held only 5-20% of unique traders. This stark contrast with OpenSea (25-35% volume, 30-40% traders) shows Blur's vulnerability to whale behavior, risking steep volume drops if big players exit.

- Farmers exiting Blur also sparked a TVL nosedive from a 26K peak to 16K ETH (-38%) in 25 days, which impacted sentiment and thinned liquidity, causing the blue-chip NFT floor price index to dip by -38% from highs to lows. Yet post-exodus, prices stabilized (+10% from lows), hinting at a return to potentially bullish organic trading.

- 💦🔬 Tx-Level Alpha: On June 17, right before Blur's Season 3 ended, cbb.eth executed a large withdrawal of 5550 ETH from the Blur Pool, which accounted for over 10% of the protocol's TVL at the time. This transaction, the largest in 90 days, underscores Blur's dependence on whale behavior. Such actions can sharply change the spread between ask and bid prices, reduce liquidity depth, and impact market stability and trader confidence, leading to volatility in price and trading activity, as we saw in the months of June & July.

👥 Brandyn Hamilton | Website | Dashboard

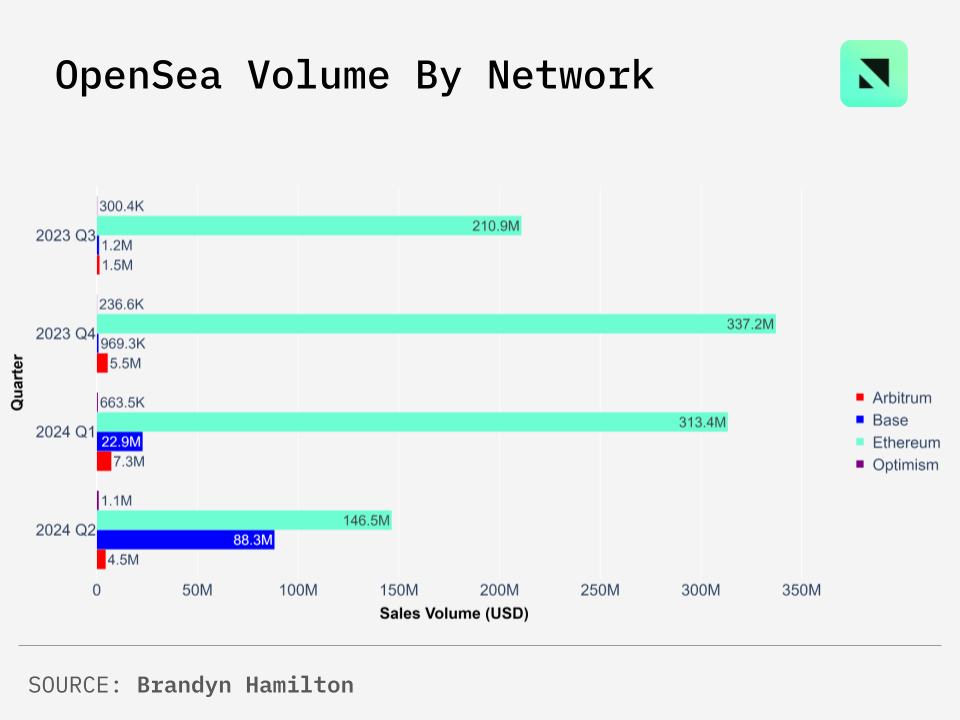

- Crypto enthusiasts and casual observers alike are likely familiar with OpenSea, the leading NFT marketplace. However, fewer may be aware of the sudden and drastic shift in usage from Ethereum Layer 1 (L1) to Layer 2 (L2) networks over the past few months. The L2 blockchains—Optimism, Arbitrum, and Base—accounted for 39% of sales volume on OpenSea in Q2 2024, up from a mere 8.9% of sales volume in Q1 2024. Notably, Base makes up the vast majority of L2 volume at $88.3M.

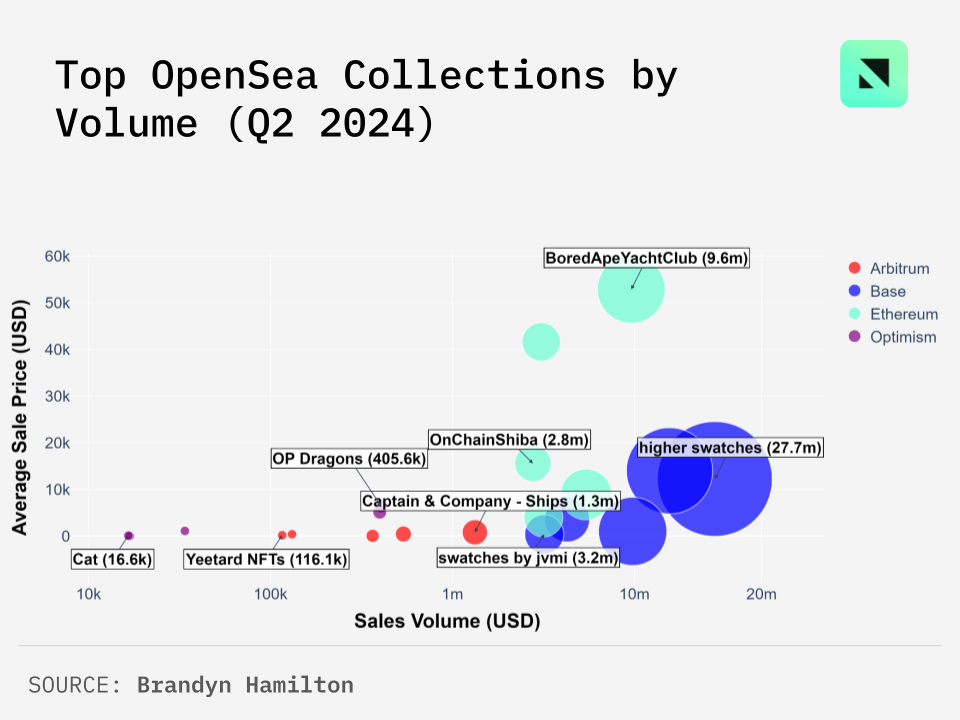

- Looking into the top 5 NFT collections on L1 and L2 networks, we see that Q2 was dominated by Base, with the top collection by volume being Higher Swatches at $27.7M. Still, L1 commands the highest average sale price per NFT, with BoredApeYachtClub reaching an average sale of $52.85K per NFT.

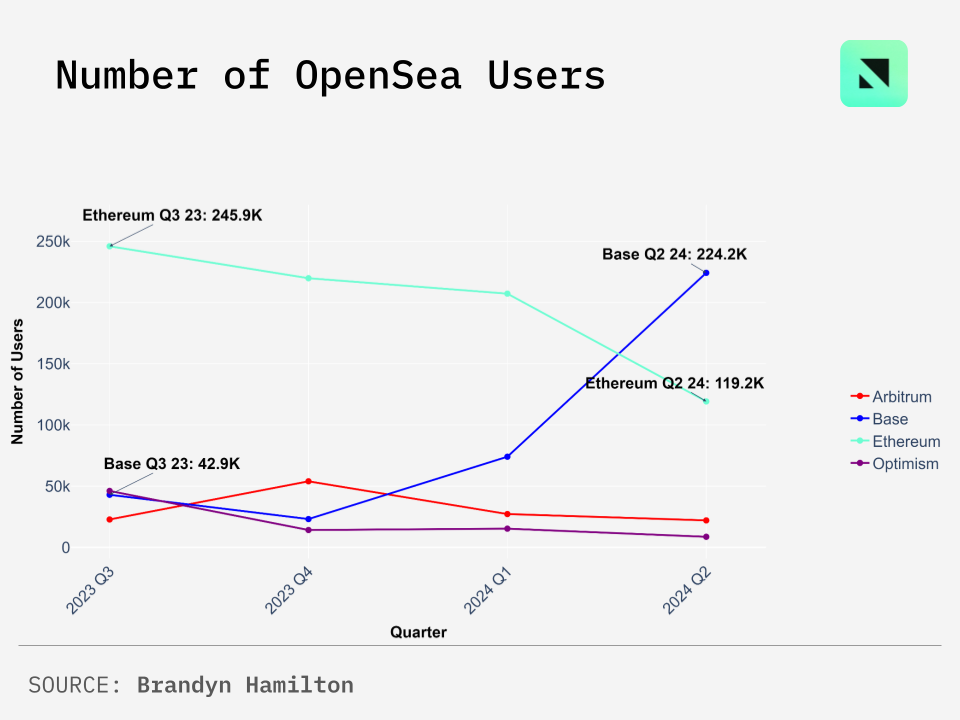

- Platform users have also surged on L2s. Users on Base outpaced those on Ethereum by over 100K in Q2. It will be intriguing to see if Base keeps up this pace, especially with Onchain Summer 2.0 having kicked off in June. Despite being newer than the other L2s, Base dominates in both users and volume.

- 💦🔬 Tx-Level Alpha: Among the top collections on Optimism in Q2 2024 was 3DNS, the first onchain domain registrar compatible with both web2 and web3. 3DNS-powered domains can be used to set email and website records, as well as send and receive crypto. The highest sold domain to date is watch.box, which sold via offer on May 6, 2024, for 23.59 ETH / $73,644. Given that the collection is less than a year old, these are some of the very first web3-enabled DNS domain sales, marking a truly historic milestone.

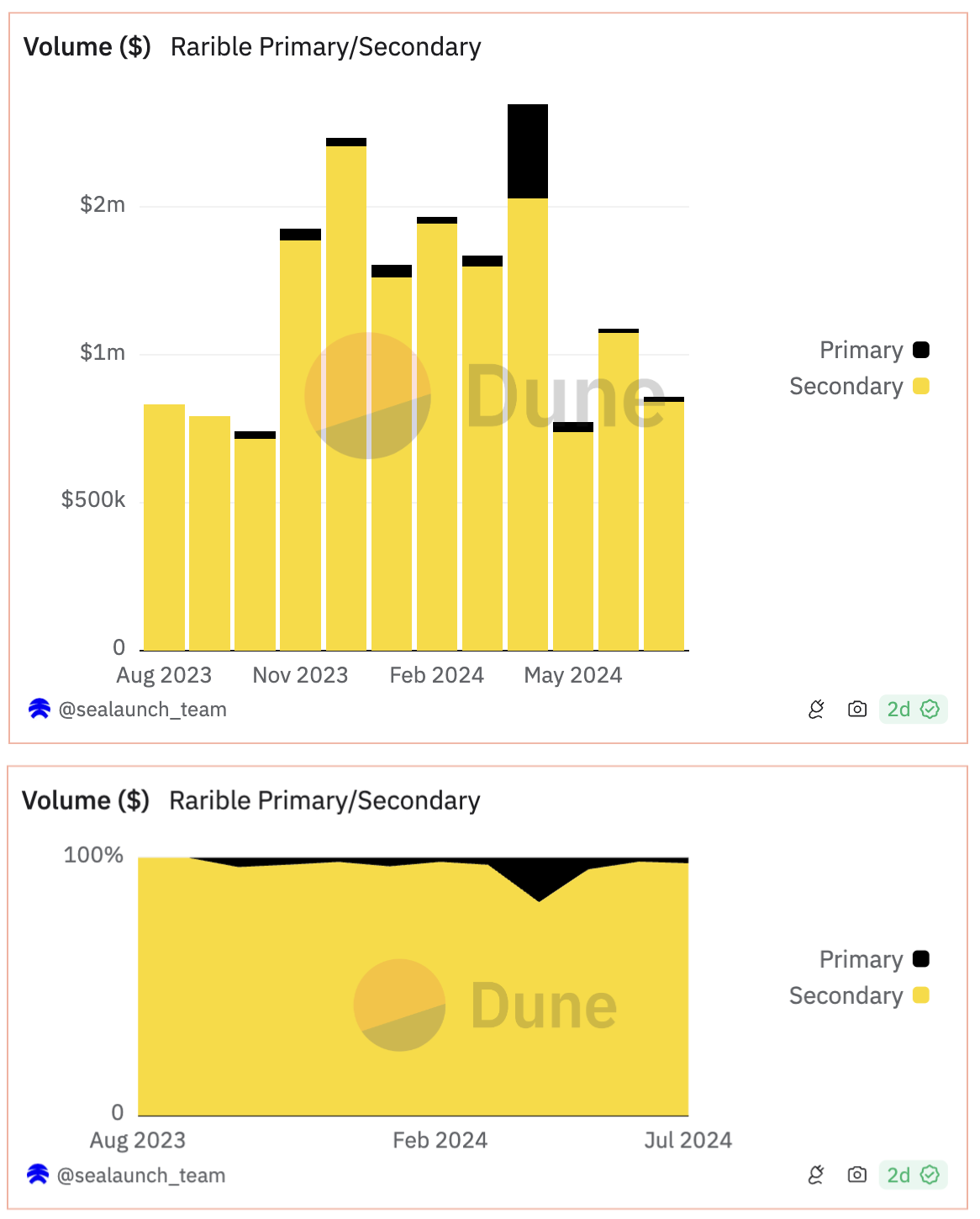

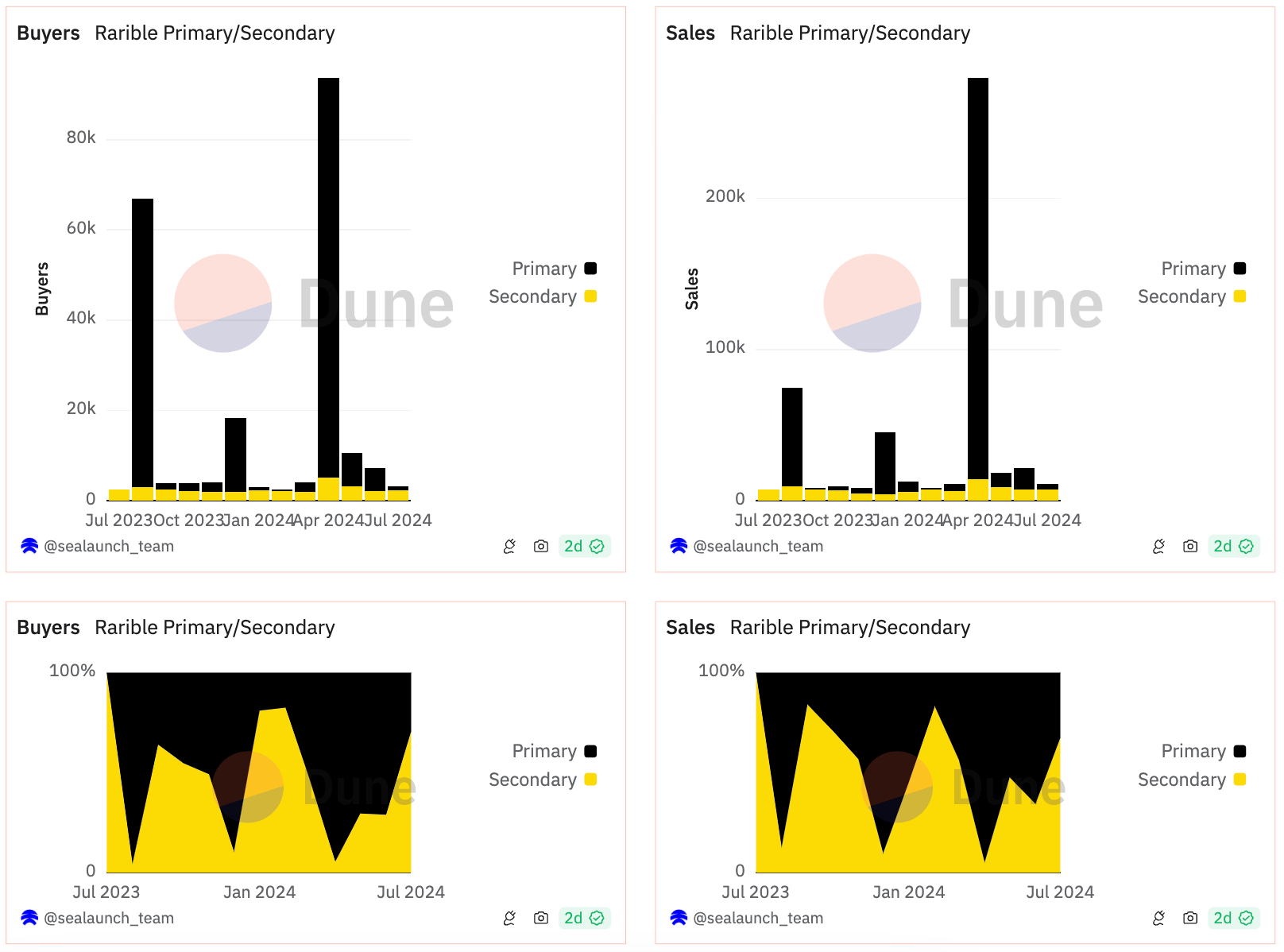

- Rarible's product suite has expanded beyond Rarible Marketplace (secondary NFT marketplace) to include: RaribleX (NFT marketplace-as-a-service), NFT infrastructure with Rarible API and also Rarible Drops (multi-edition NFT launchpad). In terms of sales volume, most of Rarible GMV still occurs in the Rarible Marketplace (secondary market), which represents about 90% of total.

- On the other hand, Rarible Drops (primary market), which allows creators to launch multi-editions NFT across multiple chains using Rarible, has successfully attracted a significant number of NFT minters representing +80% of the total users and transactions.

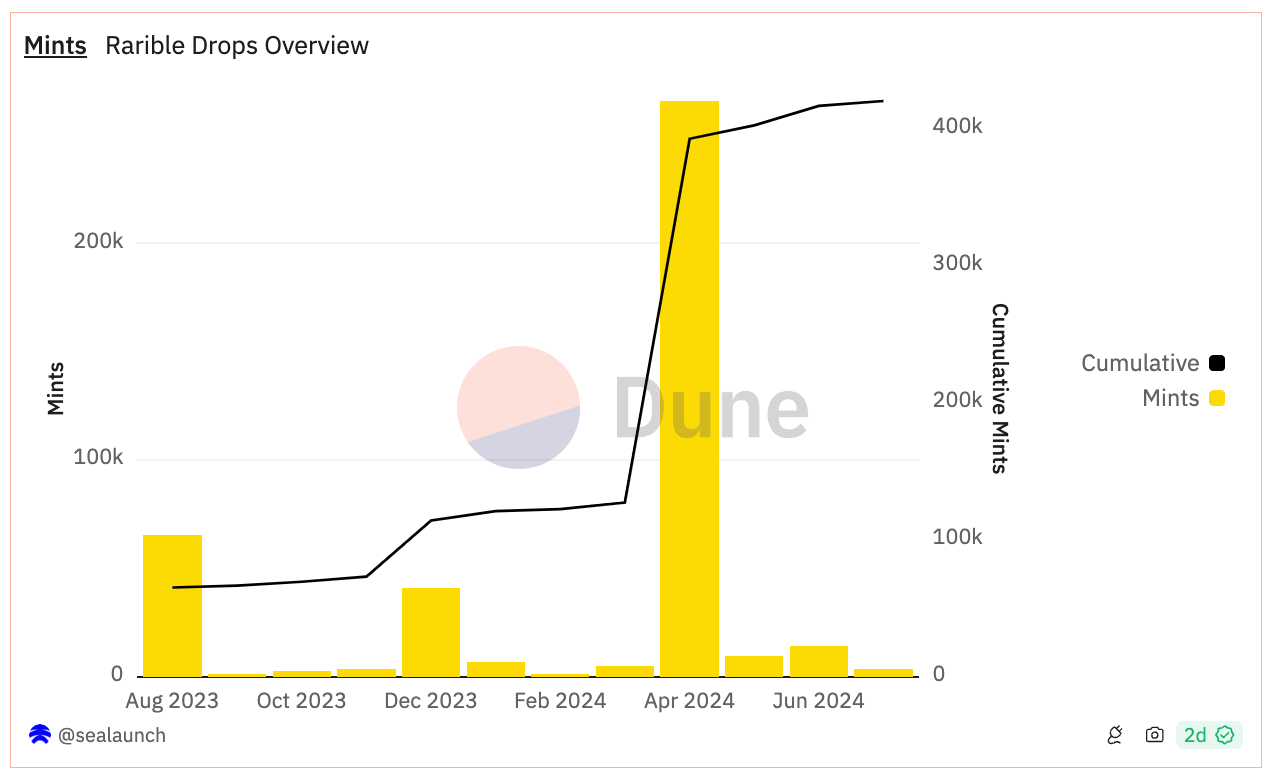

- In the last 6 months, Rarible Drops reached more than 500k mints, by more than 170k unique collectors across different chains (Ethereum, Polygon, Celo, Rari and Base), generating more than $290k in mint revenue. One of its most successful launches was “Anticipation (of a future event)” which created a spike in the number of mints on April 24, resulting in more than 190k mints by +48k distinct users.

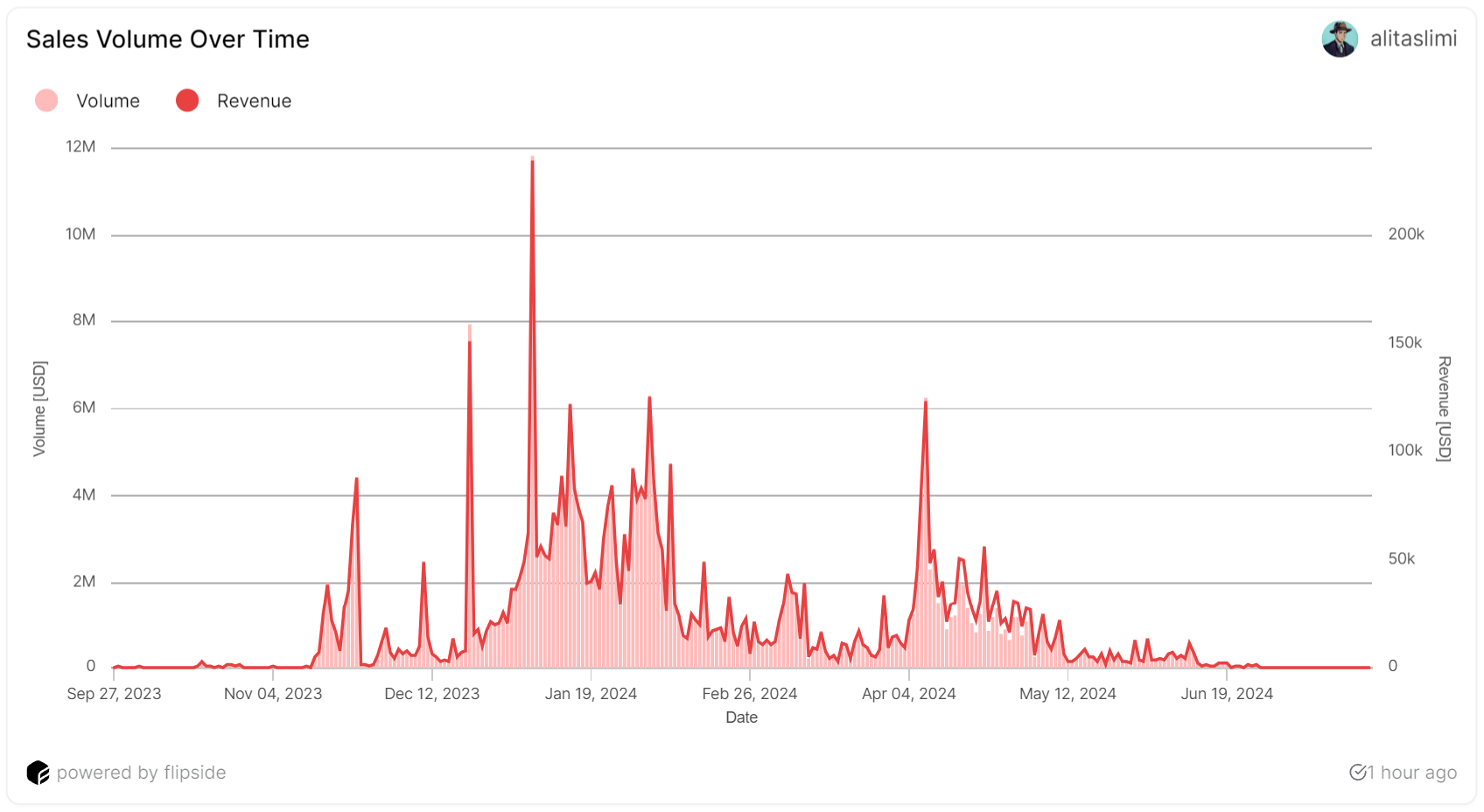

👥 Ali Taslimi | Website | Dashboard

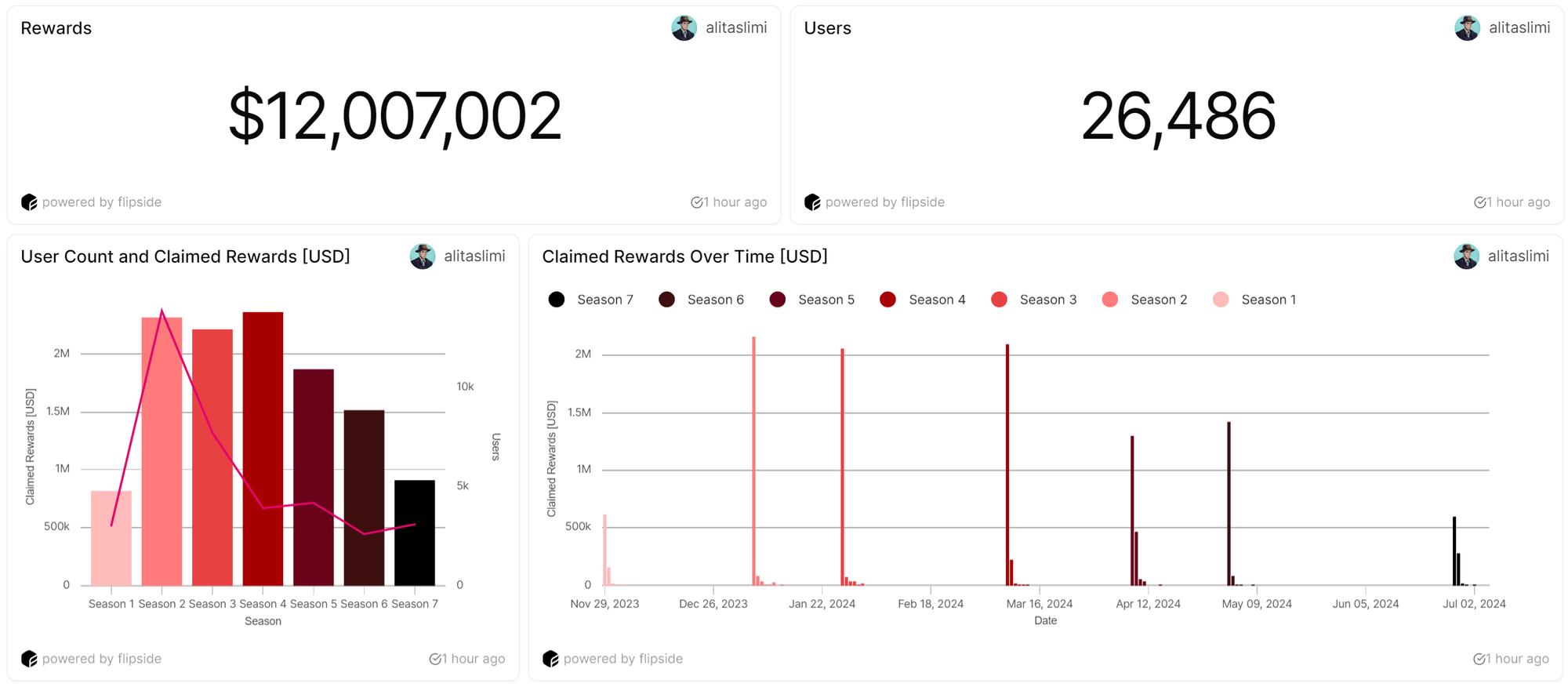

📈 Hyperspace users on Avalanche earned $12M in rewards, while the marketplace only generated $6M in revenue

- Hyperspace experienced a drastic drop in activity, plummeting from processing millions of dollars in volume to barely reaching $10,000 per day, following the announcement of the termination of their rewards program in June. Over the past few months, many NFT marketplaces have experienced a significant decline in activity after discontinuing their incentives. Although the promise of airdrops or rewards initially attracts users, these incentives do not seem to foster loyal and long-term engagement.

- Users of the marketplace earned $12M in rewards over seven seasons. With the generated revenue totaling approximately $6M, a significant portion of the reward program was reportedly funded by Ava Labs, casting doubt on its long-term sustainability.

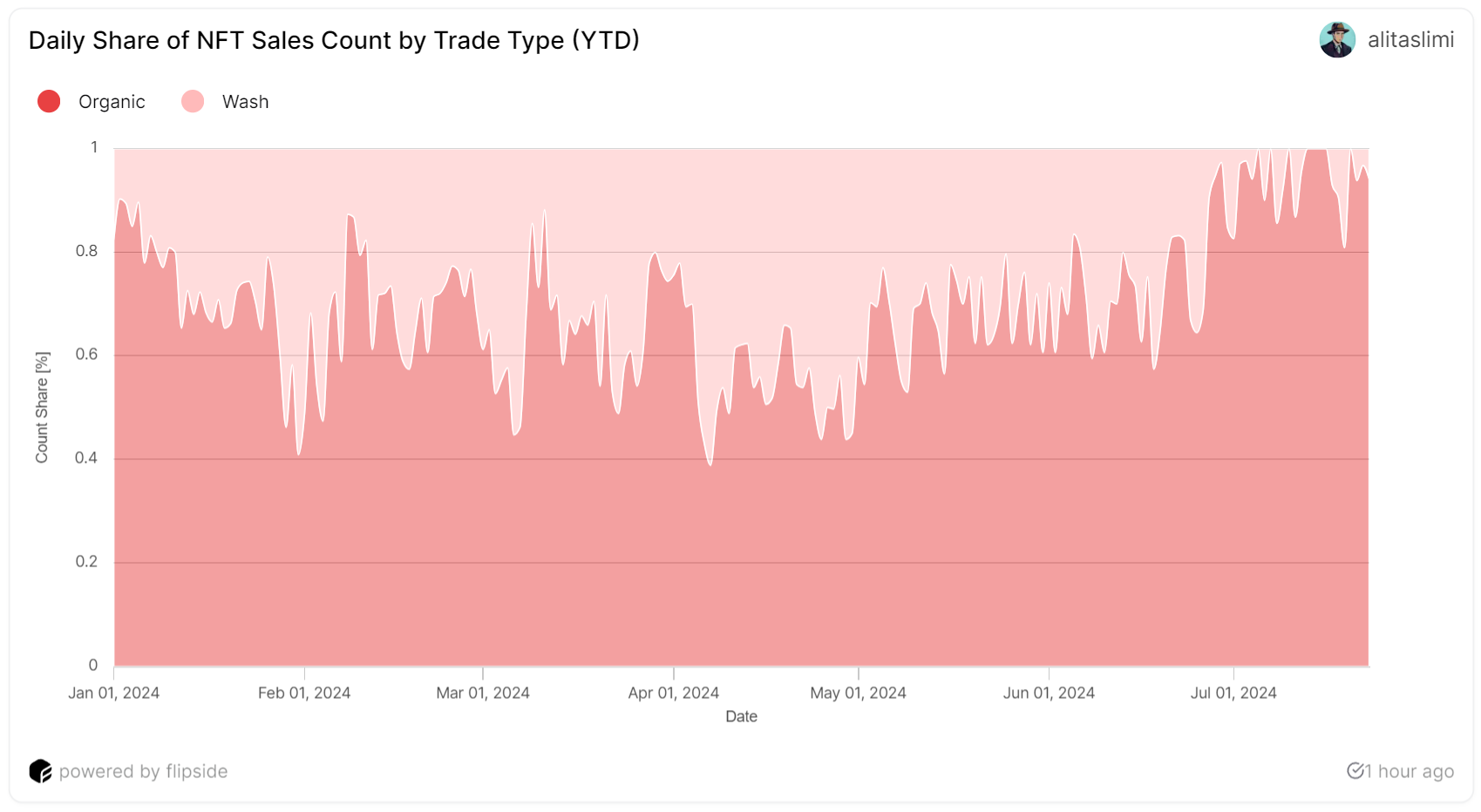

- Since the start of 2024, a significant portion of NFT sales were wash trades, which negatively impacted the reward program. Any incentives could lead to farming-like activities, which might be another catalyst for the termination of the program.