ON–011: Ethereum

Mar 5, 2020

Welcome to Issue #11 of Our Network, a weekly newsletter where top blockchain projects and communities share data-driven insights and advanced metrics.

One common criticism of crypto metrics is that they are too easily gameable.

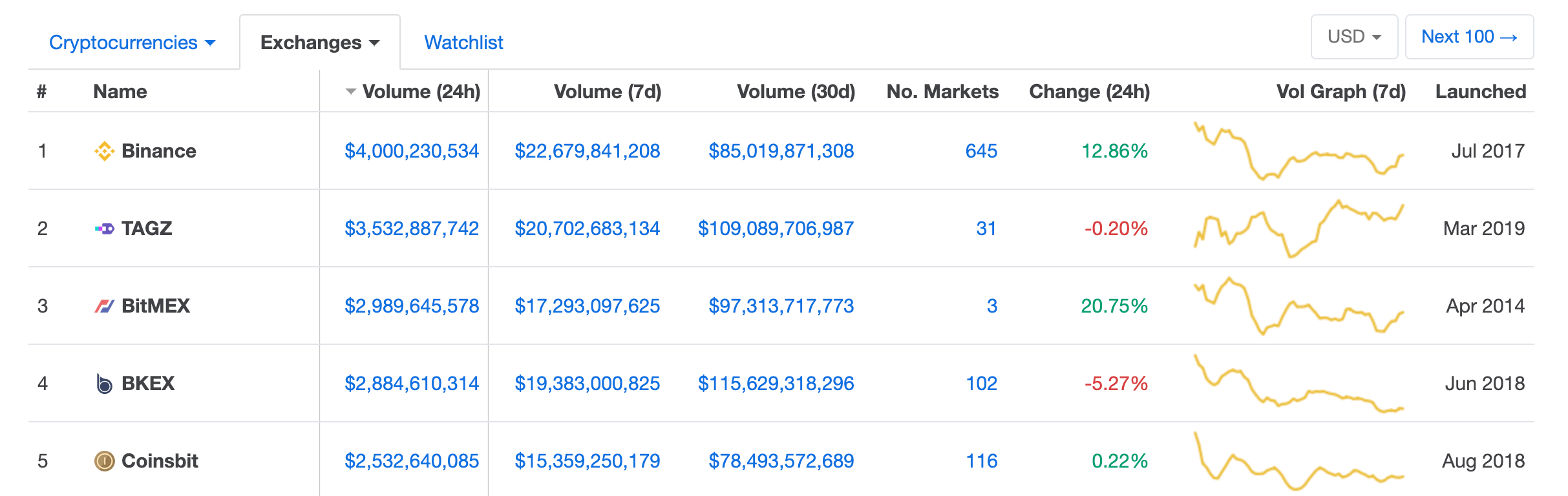

This is true to some extent. Because there are huge incentives for crypto companies to juice their numbers, it happens a lot. For an example of this in the wild, look no further than the list of top exchanges by volume on CoinMarketCap:

When you look at the full list, you will notice a number of “top” exchanges that you’ve likely never heard of before. These are not sleeping giants on the other side of the world, beating out heavyweights like Coinbase and Huobi. They are simply small exchanges that are gaming their volume numbers so they appear on this list. It makes sense — CMC is the #534 website in the entire world (source), which means it’s a great source of referral traffic.

How do you game trading volumes? There are a few methods with varying degrees of legitimacy that these exchanges employ:

- Transaction mining

- Zero-fee trading

- Wash trading

Metric gaming also happens frequently on public blockchains in order to give the appearance of a healthy network, which is a positive indicator for price.

Gaming is obviously problematic and something we should be aware of, but it doesn’t mean we should write off all crypto data as poor. It just means we need to approach metrics and lists like these with a healthy dose of skepticism. We also need to be rigorous with our methodologies in order to stay ahead of the gamers.

There is much signal when you sift through the noise.

This week our contributors provide data-driven coverage on the world of exchanges:

- ETH on Exchanges

- 0x

- Uniswap

Contributor: Alex Svanevik, co-founder at D5

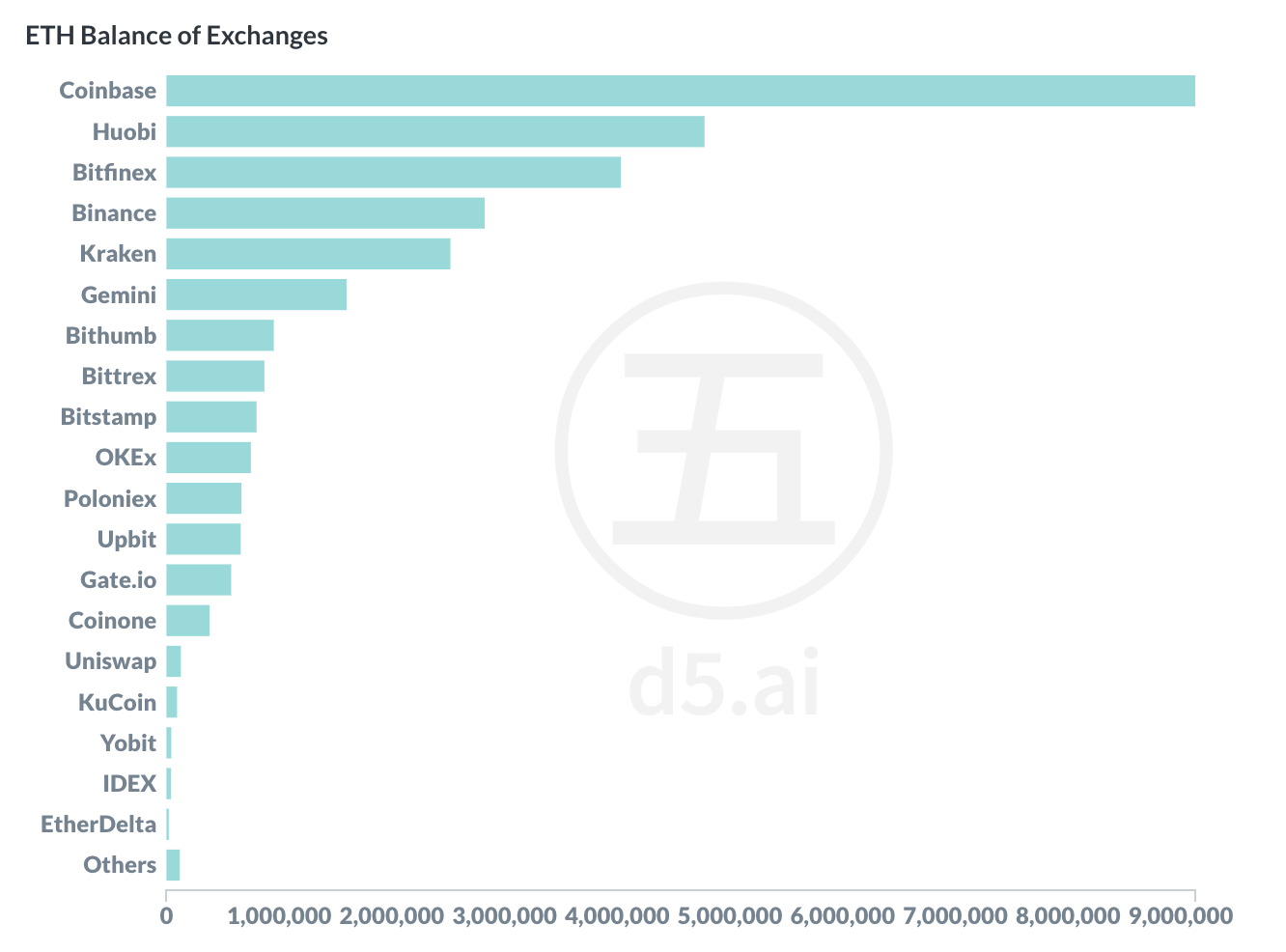

- More than 31M ETH is held in exchange wallets. This includes centralized exchanges such as Coinbase, plus decentralized exchanges such as Uniswap. For context, the commonly reported "ETH Locked in DeFi" is currently sitting at 2.9M ETH. In other words, there's more than 10X the amount of ETH "locked" in exchange wallets than in DeFi.

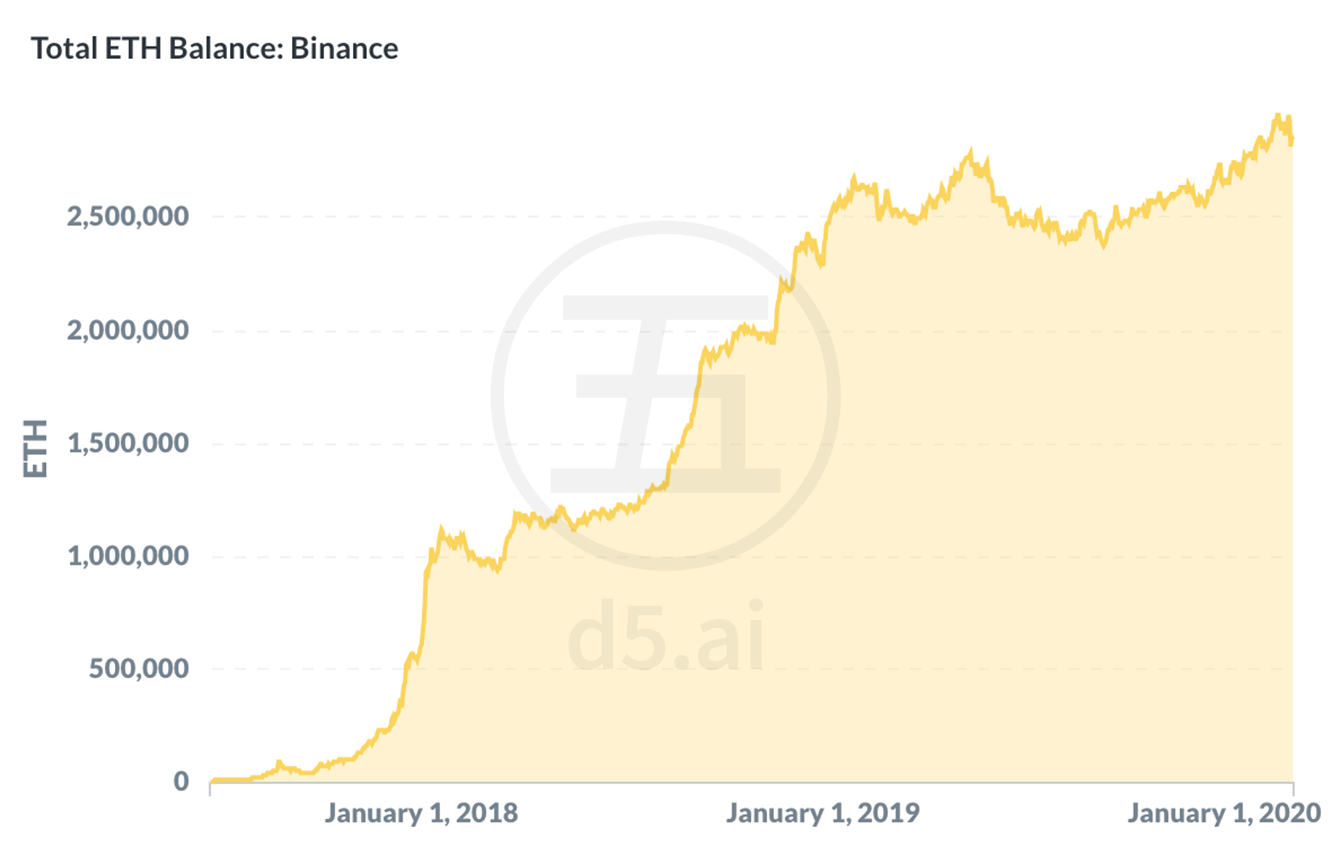

- The vast majority of this ETH is in centralized exchanges, with Coinbase, Huobi, Bitfinex, Binance, and Kraken holding the most (above [fig. 1]). Drilling down on the full history of Binance (below [fig. 2]), we see how the exchange quickly hit its first 1M ETH right at the crypto peak of January 2018.

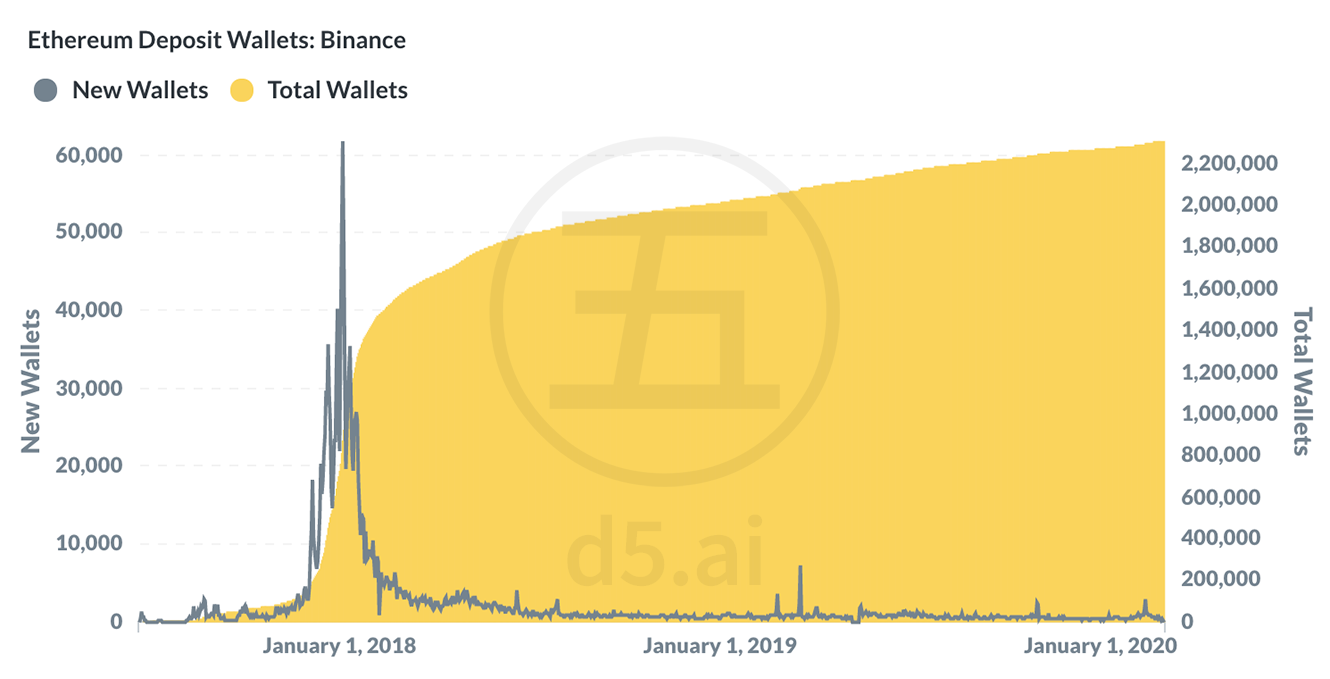

- The millions of deposit wallets associated with exchanges can serve as proxies for their growth metrics. Binance will normally provide one single address per retail customer, which means that new deposit wallets (below [fig. 3]) is likely to correlate with the number of new exchange customers. Again we see that the largest influx of customers was around the peak in January 2018. Conclusion: Binance's growth in the last 18 months has likely come from 1) existing customers, and 2) non-Ethereum cryptoassets.

Contributor: Caleb Sheridan, co-founder of Blocklytics

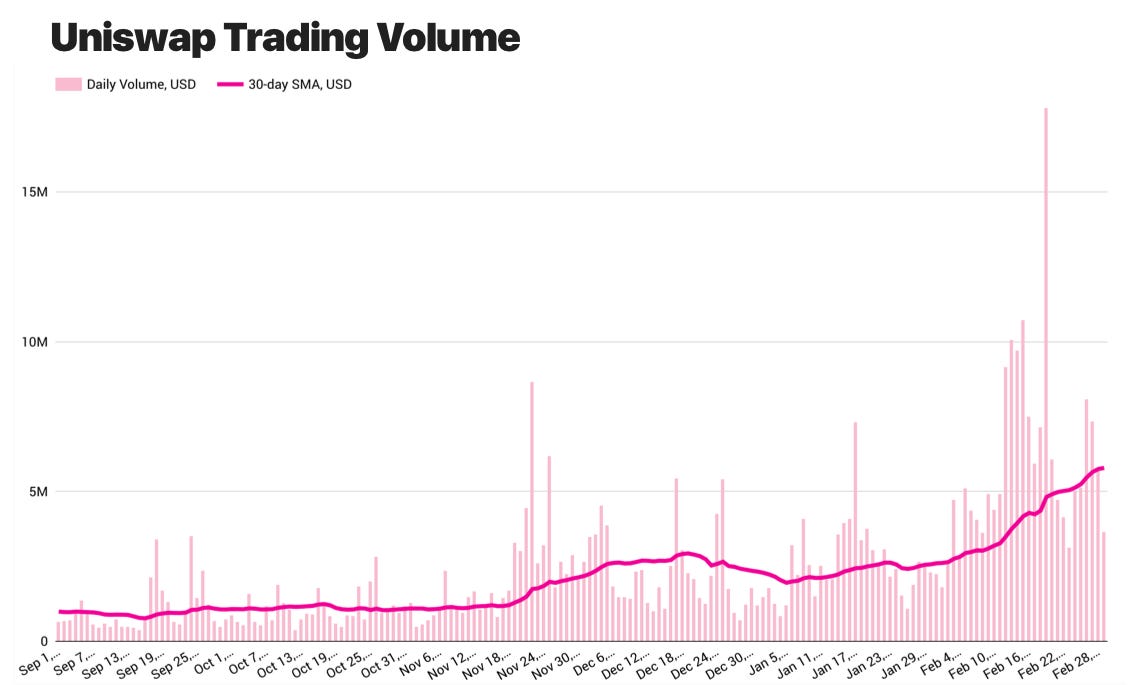

- February's volatility has been great for Uniswap's trading volumes. The 30d average daily volume is now over $5m.

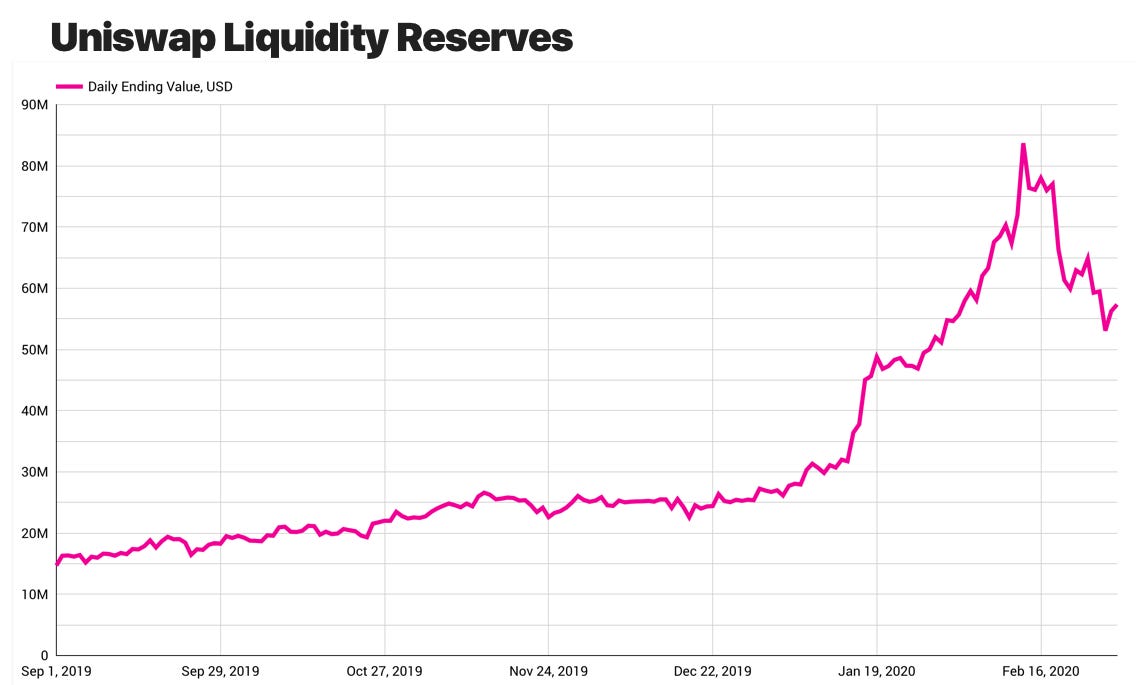

- Liquidity reserves saw a sharp drop in both USD and ETH. The drop is due to recent ETH price action and liquidity being removed from the MKR market. This appeared to be a defensive tactic against flash loans. The liquidity has not returned despite a Maker upgrade that introduces new defense against flash loans.

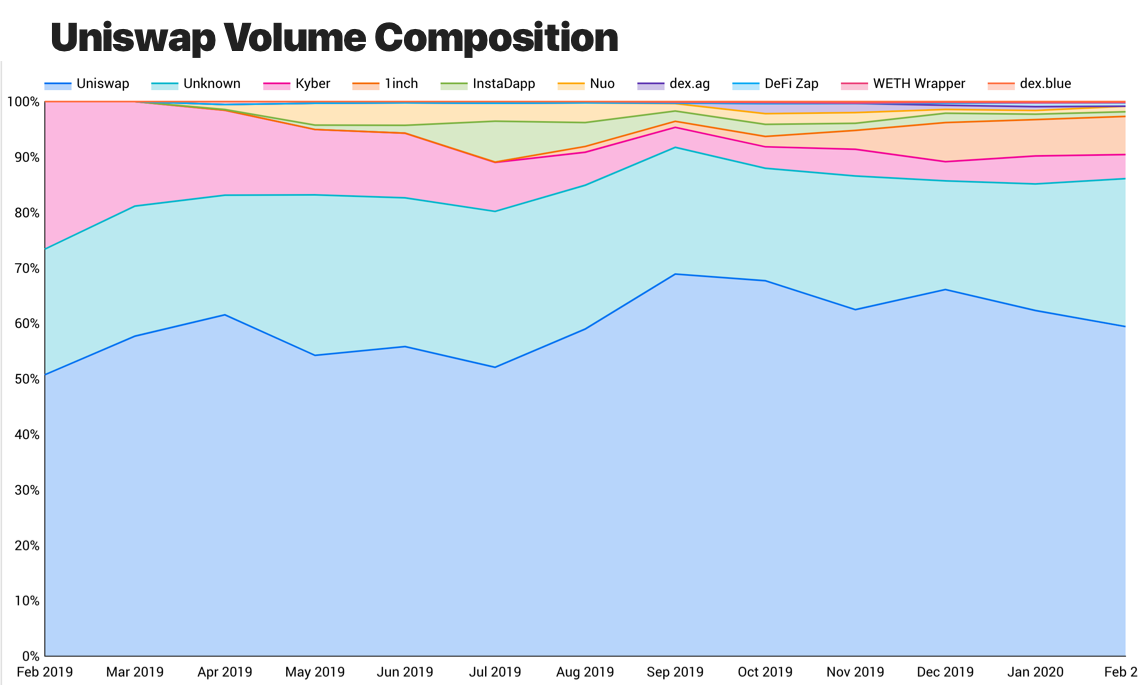

- As reported previously, other contracts drive a large amount of the volume on Uniswap. Notably, DEX aggregator 1inch is driving slightly more of the network traffic than the last time we looked at this chart.

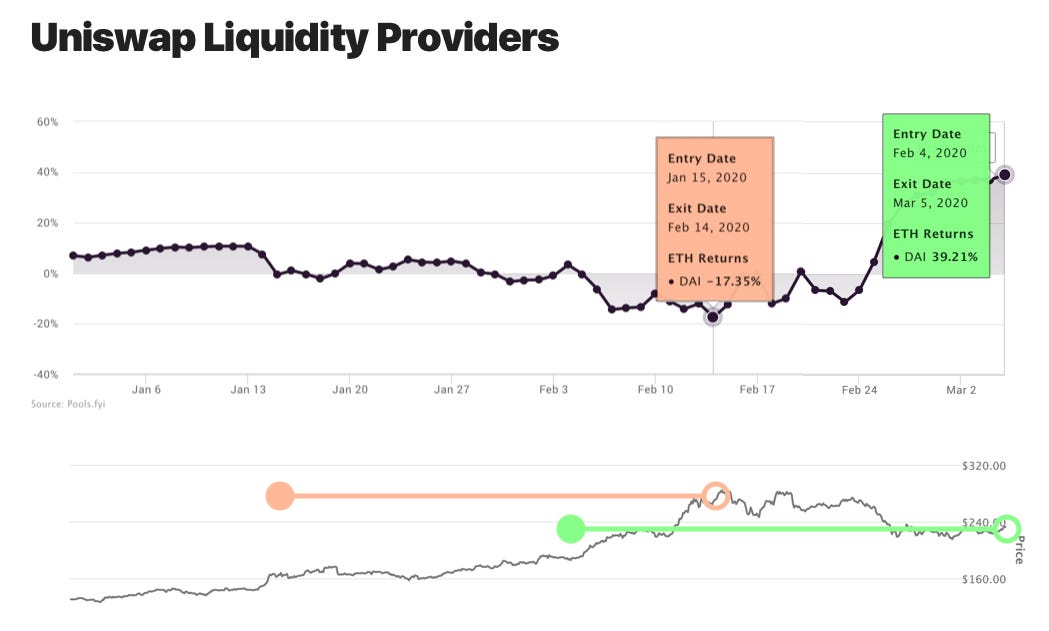

- Timing matters. Uniswap LPs win when trading fees surpass the opportunity cost of not holding ETH. This chart shows a tale of two theoretical positions. One where the price of ETH grew 75% and the LP misses out. And a second where the price of ETH grows 20% with high volatility.

Contributor: Alex Kroeger, Data Scientist at 0x

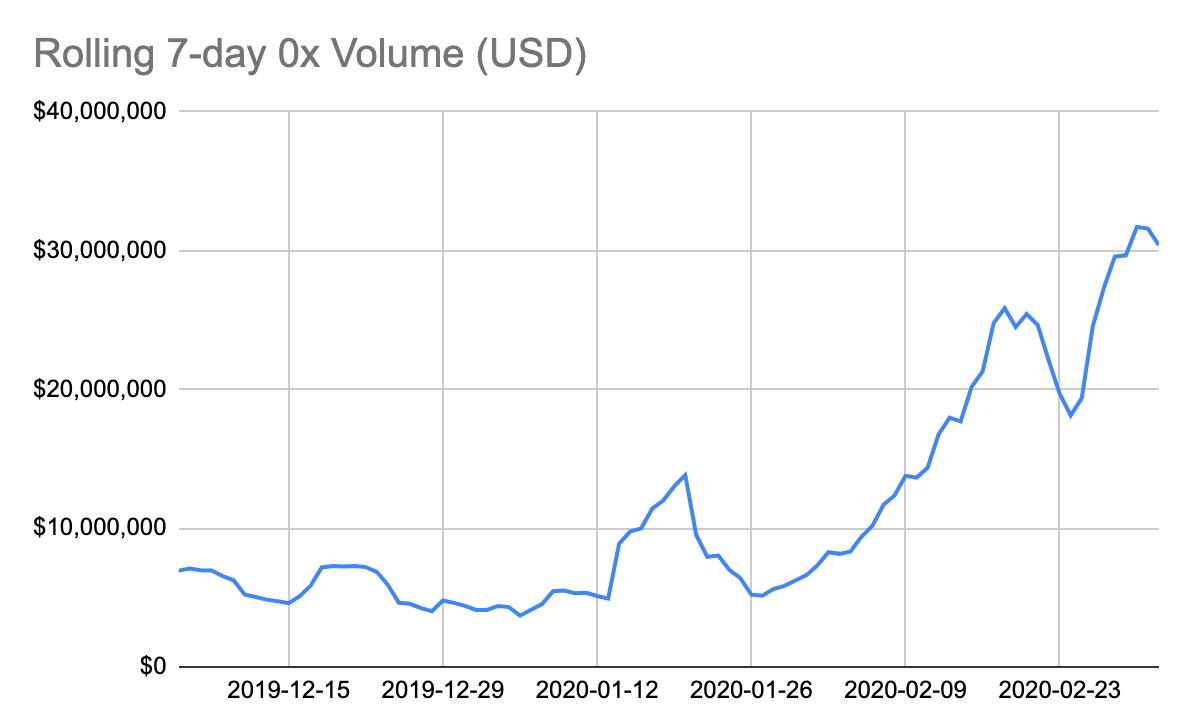

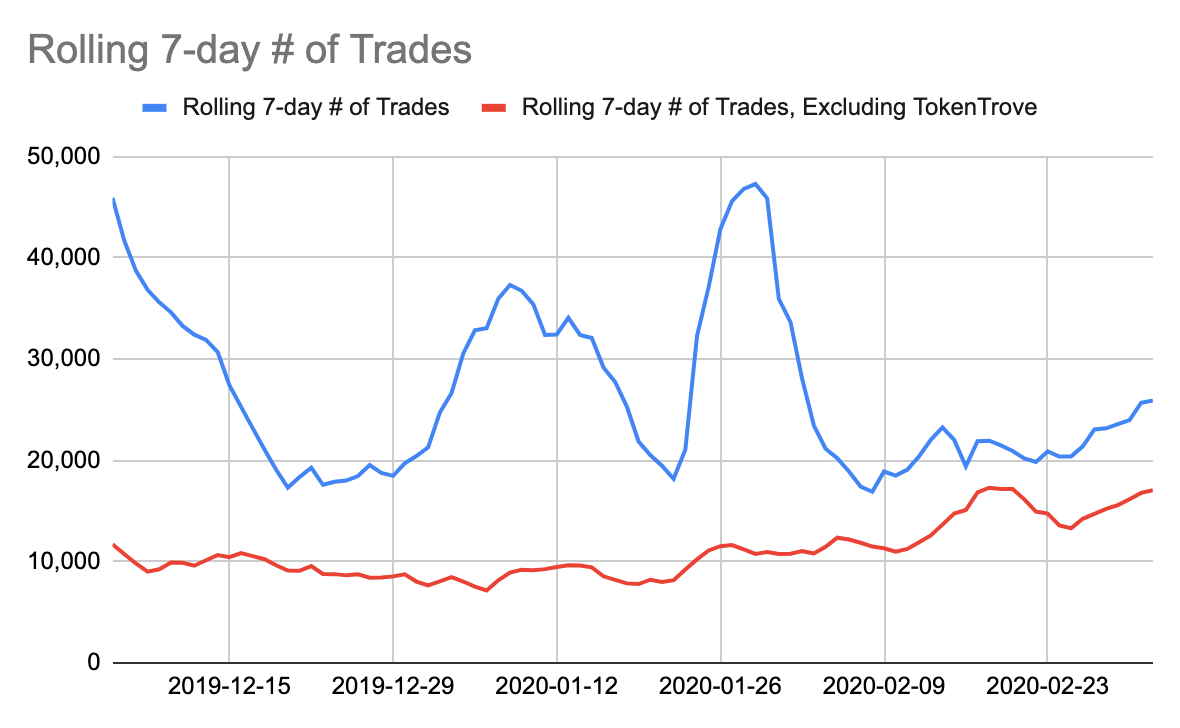

- It’s been a great month for DEXs. Overall DEX volume is up, and 0x is no exception. Over the past month, 0x weekly volume increased roughly 6x, up from ~$5M per week to ~$30M per week. Overall trade count has largely been driven by NFT trading on TokenTrove, but excluding TokenTrove there has been an increase in the number of trades taking place on the protocol as well.

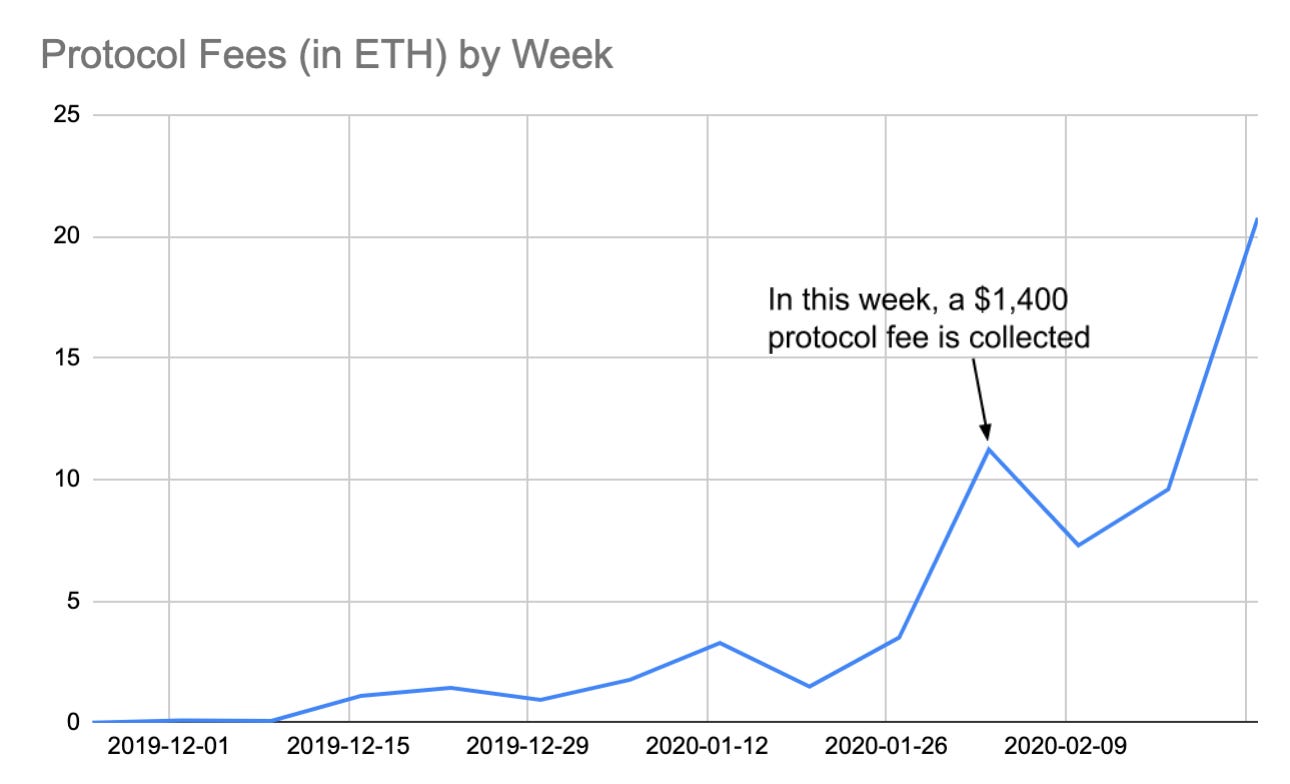

In the last update, there was a discussion the new economic incentive structure of the 0x ecosystem launched in version 3 of the protocol. An integral component of the new token economics is the introduction of protocol fees with each 0x trade, designed to align the incentives of market makers and ZRX holders with the best interest of the ecosystem.

As adoption of v3 has grown, there has been a steady increase in protocol fees collected, which are paid out to market makers and ZRX stakers at the end of 10-day “epochs.”

- The last update had a discussion of how protocol fees in 0x v3 share arbitrage profits with market makers. Shortly after that update, a large (likely errant) trade on Uniswap caused a massive DEX arbitrage opportunity between 0x and Uniswap’s ETH-DAI pool. After a gas price competition, the winning arbitrage bot paid a whopping 6 ETH (~$1,400) in gas costs and an additional 6 ETH in 0x protocol fees, showing the new token economics in action. Check out the transaction and Will Warren’s breakdown.

About the editor: Spencer Noon leads investments for DTC Capital, a fundamentals-focused crypto fund. He actively tweets about on-chain metrics.