ON–014: DeFi

Mar 26, 2020

Our Network is a weekly newsletter where top blockchain projects and communities share data-driven insights and advanced metrics.

Before we dive into this week’s issue, I wanted to share that Our Network is officially live on Gitcoin Grants!

Please consider donating if you believe in our mission of delivering free community-driven crypto analytics. All funds generated will go towards supporting three new strategic initiatives, which you can read more about on our grants page.

This week our contributors cover the following DeFi projects:

- MakerDAO

- Compound

- Aave

- Set Protocol

Contributor: Primož Kordež, Founder of BlockAnalitica

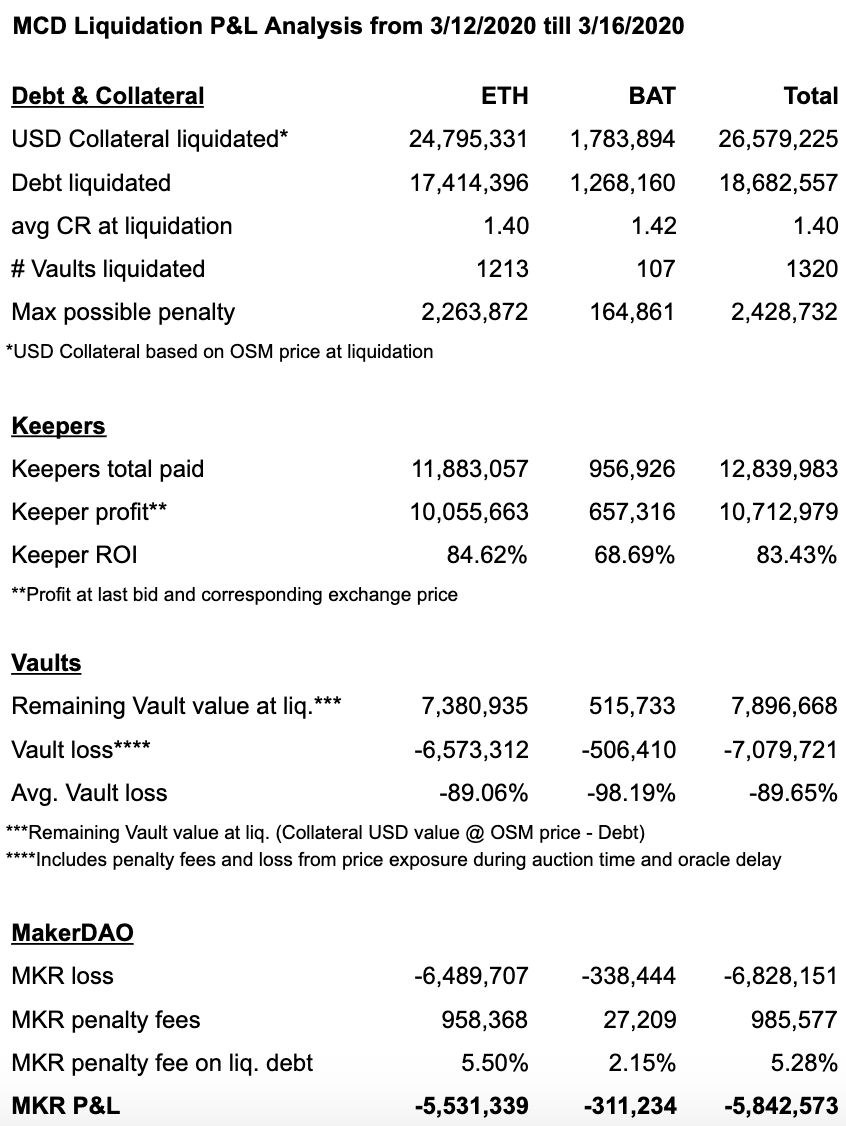

Liquidation Period P&L Analysis. Starting on March 12th, the price of ETH crashed more than 50% in less than 24 hours and caused massive liquidations on MakerDAO. Another severe ETH price drop came 3 days later, causing an additional $4.3m collateral was liquidated. The first wave of liquidations ended poorly for MakerDAO and Vault owners, as auction keepers severely underbid liquidated collateral due to reasons such as liquidity issues, low bid duration, and network congestion.

Stats during this period of extreme volatility from March 12-16:

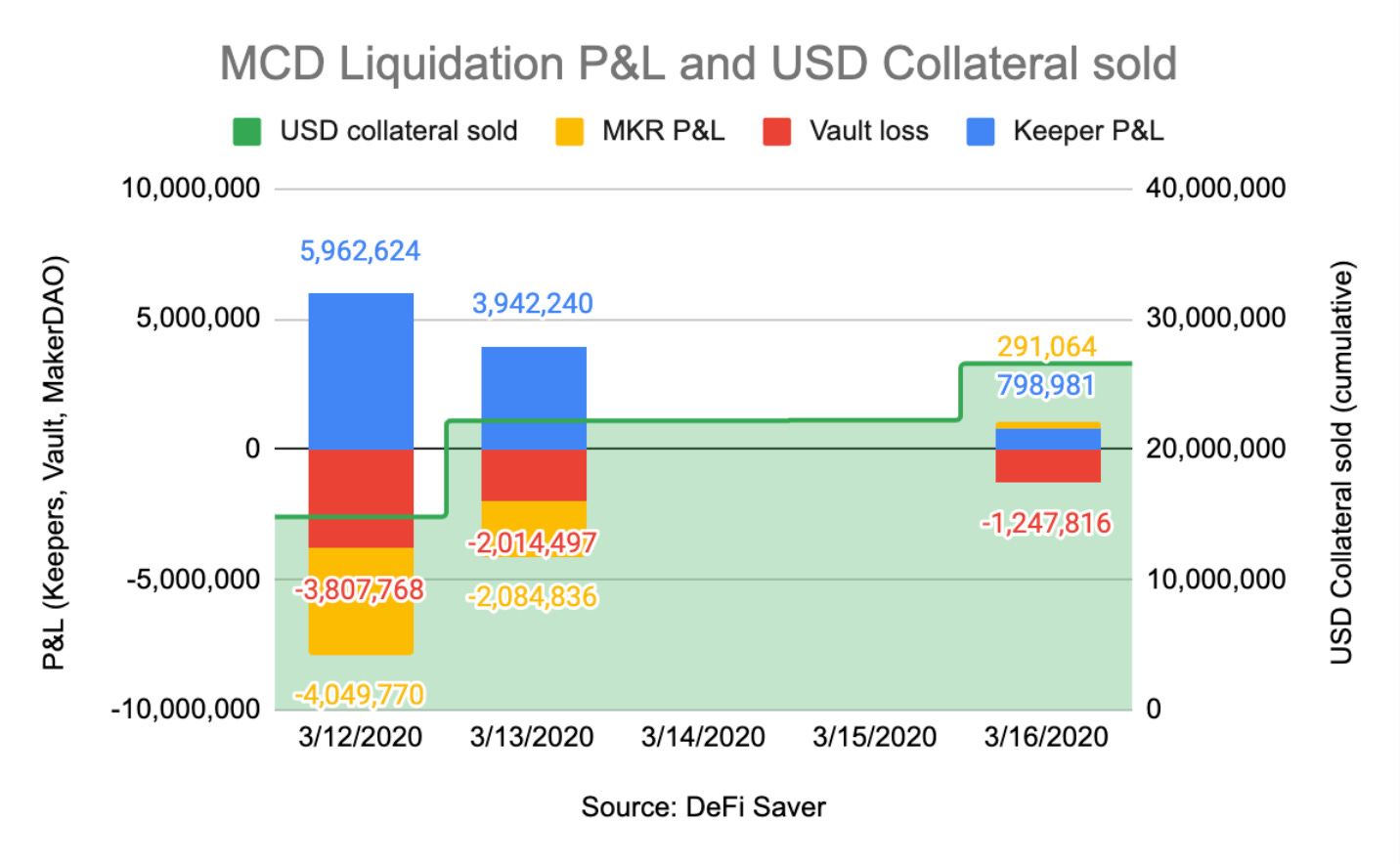

During the 3 days of liquidations, Maker lost $5.8m and Vaults lost $7.1m (or 90% of remaining collateral value), while Keepers earned $10.7m (83% ROI). Note: the difference between the higher overall loss vs. total profits is due to falling prices during the auction duration as well as an oracle price delay. Also, Vault losses include penalty fees and price exposure loss during auctions for their remaining collateral.

The loss for Maker equals 2.3x its yearly burn rate if we extrapolate the first 3 month of MCD net revenue cashflow ($624k). The Maker system also lost more than it has earned since inception, as total MKR supply after debt auction has now surpassed 1m MKR.

If auctions would have worked as planned (i.e. bid from keepers would be at least 13% above all debt that was liquidated), Maker would have instead earned $2.4m in penalty fees and incurred zero loss. That said, Maker still earned almost $1m in penalty fees on some loans.

While most of the losses came from ETH-collateralized Vaults from March 12-13, there was also an insignificant amount of losses generated on March 16 from BAT-collateralized loans. On that day, keepers bid ~50% below debt value as BAT’s price and liquidity worsened heavily. Losses from BAT loans amounted to $340k for Maker and $410k for Vault owners.

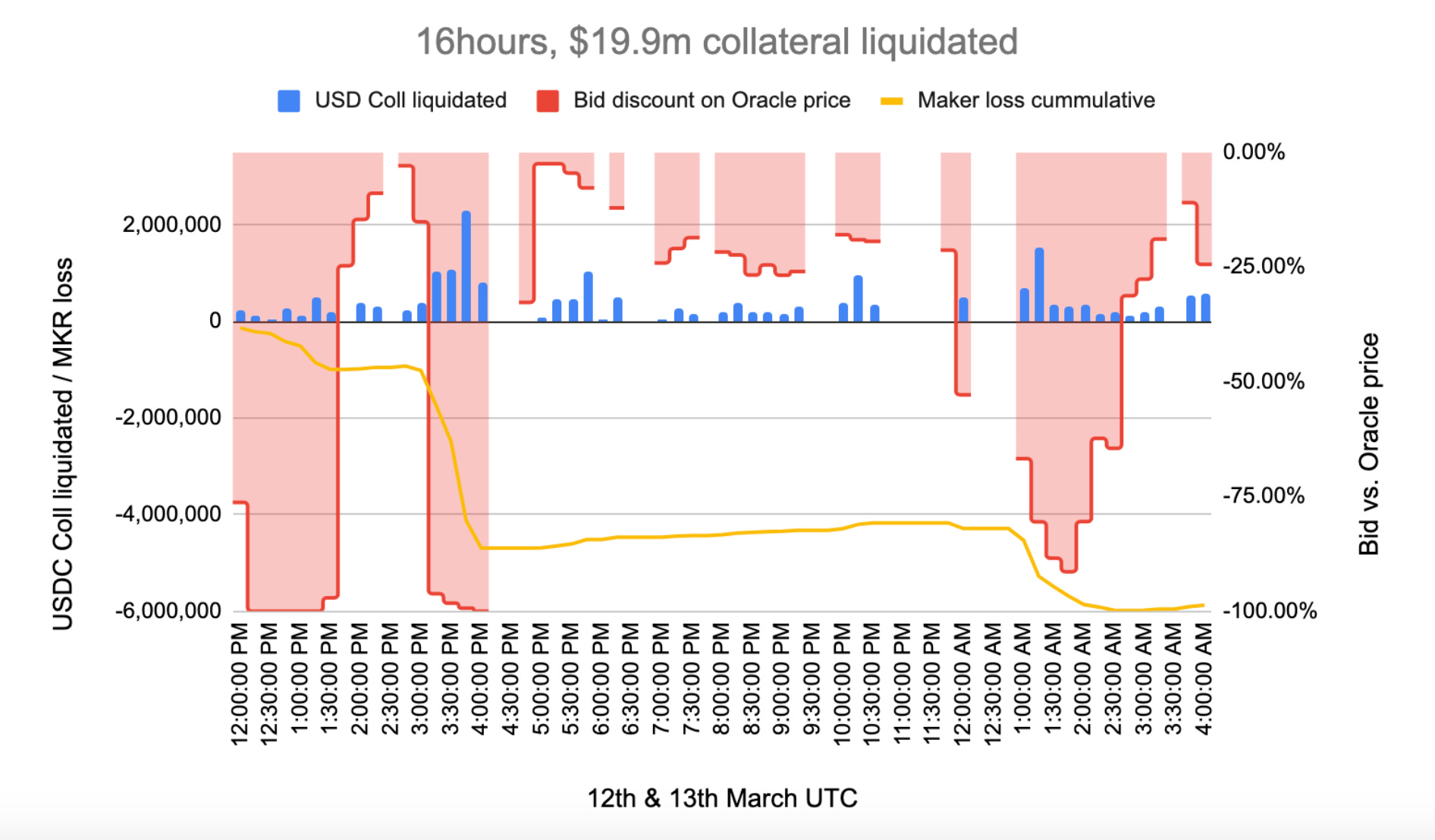

Dai Peg & Liquidity Issues. A lack of Dai liquidity was one of the main reasons that the liquidation auctions ended poorly. Even if everything else worked as planned, it is questionable whether keepers would have been able to source 22m DAI in less than 24 hours to protect Maker and Vault owners from losses.

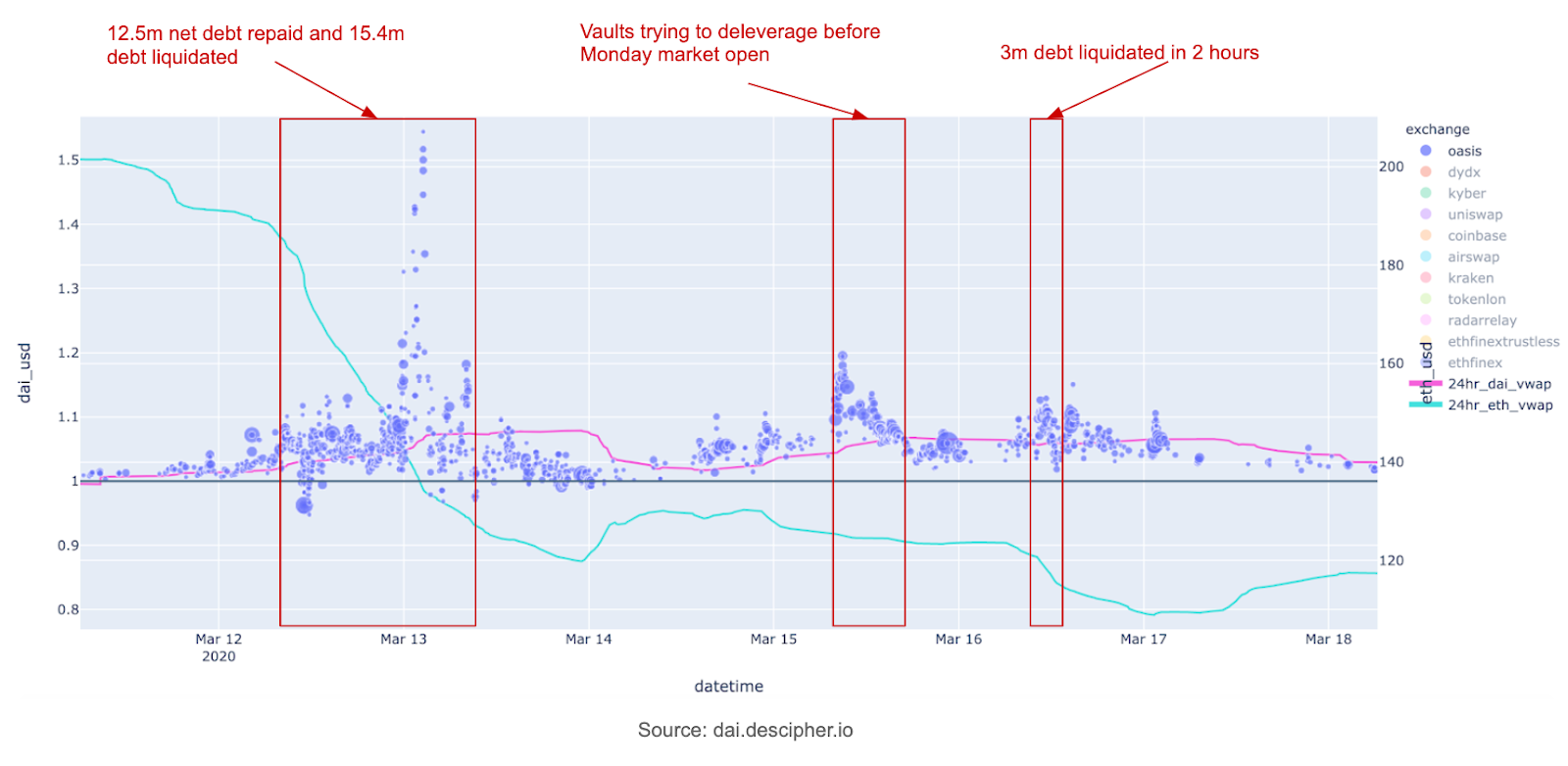

This was also one of the reasons Dai experienced heavy price appreciation and traded above $1.1 even before the auctions were triggered March 12th, as Vault owners were searching for Dai to close out their CDPs. On the first day of liquidations, Vaults repaid a net 12.6m Dai, which was the largest unwind of positions ever seen in MCD. This significantly reduced the number of future liquidations, and had this not happened the sheer amount of total debt could have been catastrophic for the protocol. DeFi Saver alone managed to protect 4m of debt from getting liquidated.

The chart above shows how Dai price was appreciating during the time when Vaults were deleveraging and auction keepers were acquiring inventory to bid in auctions. The other reason that the price of Dai increased during this time was because DeFi investors were flocking to it as a safe haven. It is commonly known that Dai price is negatively correlated with ETH price, but this negative correlation is even more severe when ETH price experiences large drops. To illustrate, Pearson correlation coefficient between ETH and DAI price (both 24h rolling VWAP) for last month measures -0.82.

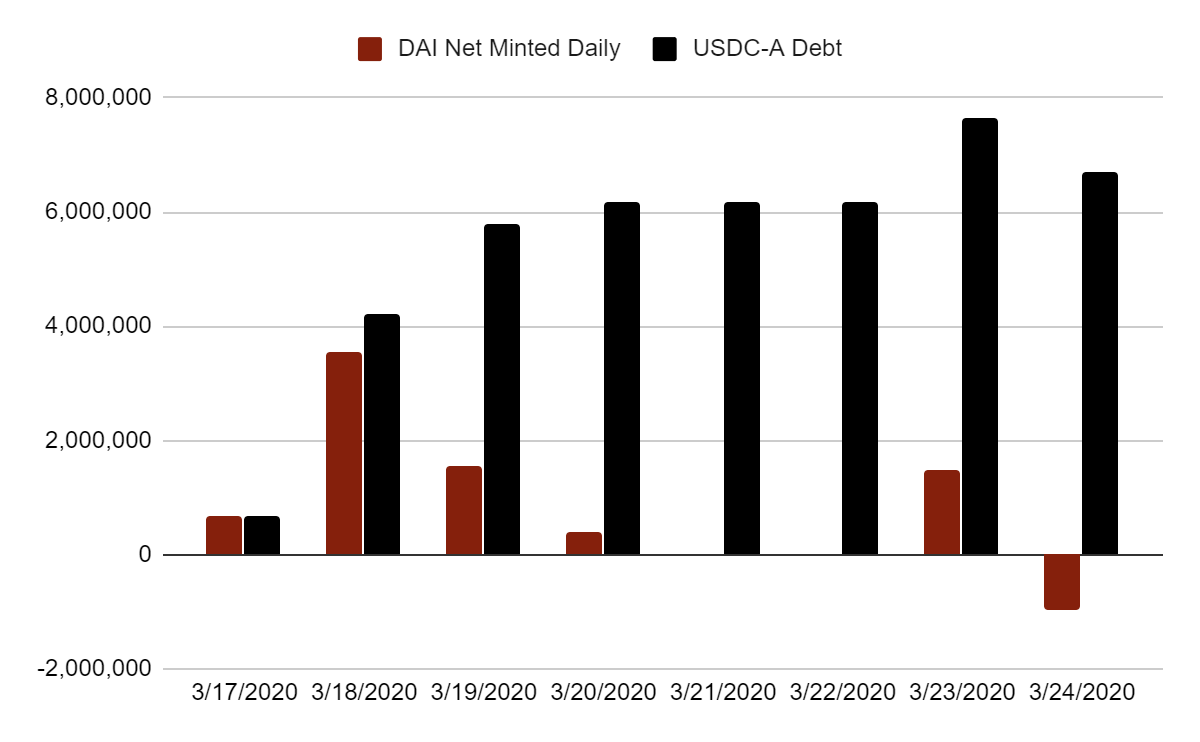

USDC-Collateralized Dai Analysis. The lack of Dai liquidity led Maker governance to perform an executive vote to onboard USDC as a third collateral asset type in advance of MKR debt auctions. This would allow auction keepers and market makers to provide sufficient liquidity to the system by minting new Dai with USDC (an asset that has a large liquidity base and does not carry ETH price exposure risk). Vault owners minted about 6m Dai in the first 3 days after it was introduced:

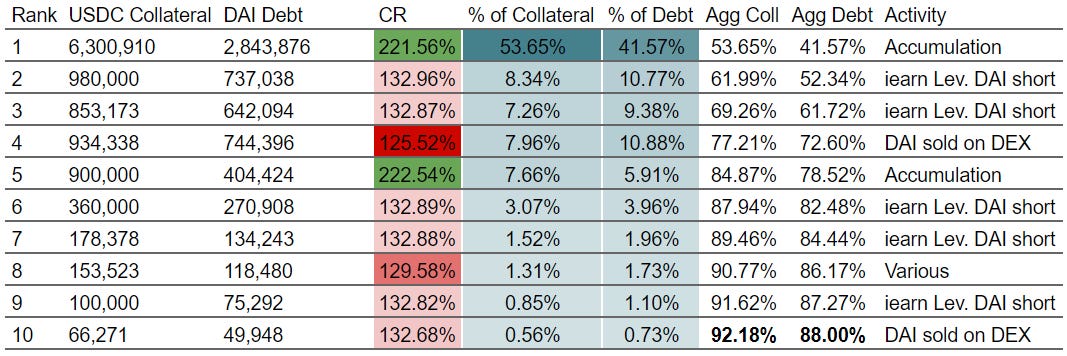

At the time of writing, there are 95 USDC Vaults open with at least 100 USDC in collateral. The total amount of USDC collateral is 11.725m, and the total debt from this is 6.838M Dai (171% collateralization ratio). It’s also worth noting that whales dominate these Vaults:

The largest Vault represents 41% of total USDC Dai debt

The 5 largest Vaults represent 78% of total USDC Dai debt

The 10 largest Vaults represent 88%. of total USDC Dai debt

On-chain analysis suggests that Vaults with higher collateral ratios are accumulating Dai and also hold some of the largest Dai debt positions in Compound. These entities might be keepers accumulating liquidity for potential upcoming collateral auctions and past debt auctions. On the other hand, many of the lower collateralized vaults opened leveraged DAI short positions by using iLeverage contracts from iearn or sold Dai on various decentralized exchanges. These entities are essentially providing liquidity and downward pressure on Dai price, which was one of the purposes of introducing USDC as a new collateral type.

As of March 24th, Dai is currently still trading above the peg at around $1.03 but the situation has improved by at least $0.02 since USDC collateral was introduced and market makers arbitraged the price. If we aggregate Dai orderbook bids above $1 across all DEX and CEX, there still seems to be 8m Dai in demand at prices above $1. However, there is also additional Dai demand not seen in order books, so the real demand might well be 2x-3x higher. This also somehow coincides with a 33m Dai supply drop since 12nd of March. It is therefore reasonable to assume that previous Dai holders were short-term holders and sold Dai because of a premium (although it is worth noting Dai demand is probably also lower because of 0% DSR and more stable ETH price.)

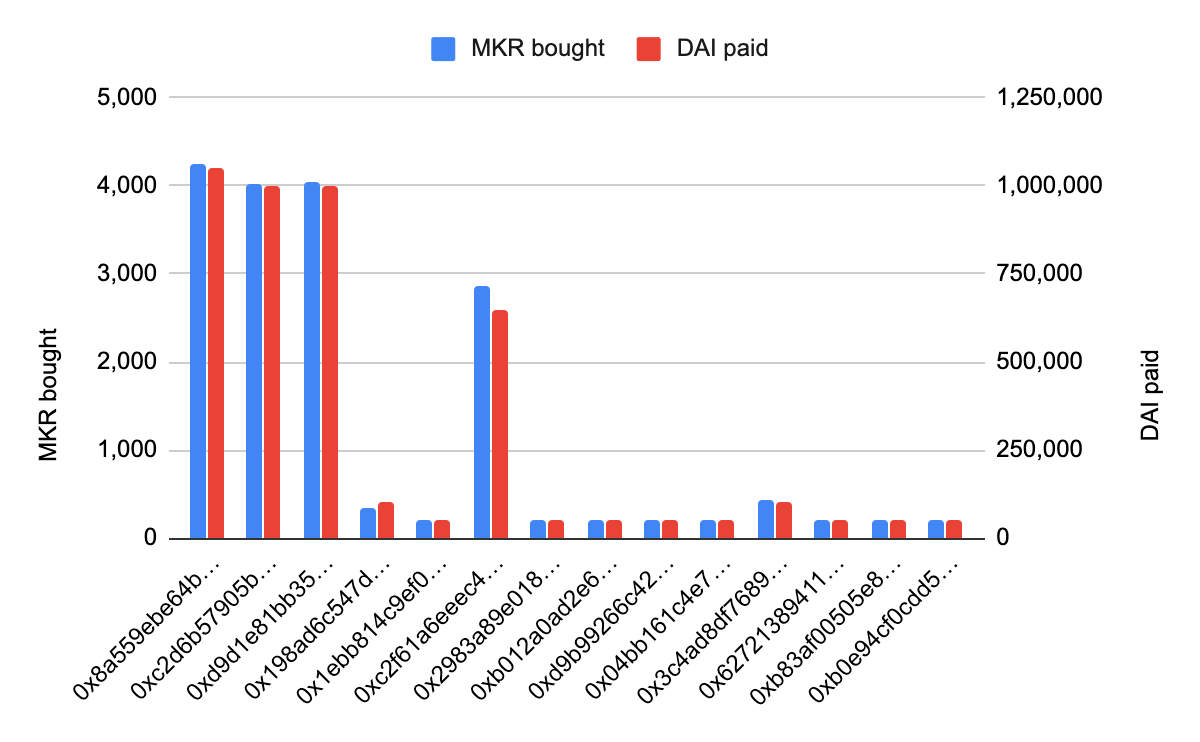

MKR Debt Auctions. As of Wednesday this week, 86 different MKR debt auctions successfully finished, recapitalizing the MakerDAO system by $4.3m. There are still 20 auctions needed (~1m Dai debt remaining) to recapitalize the system fully. Below are stats for MKR debt auctions during the period 19th till 23rd of March:

31 unique auction participants

14 unique bidders won auctions

86 auctions finished

4.3m raised / 17.630 MKR minted

Average DAI price per MKR: 243.9

Total MKR supply: 1,002,804

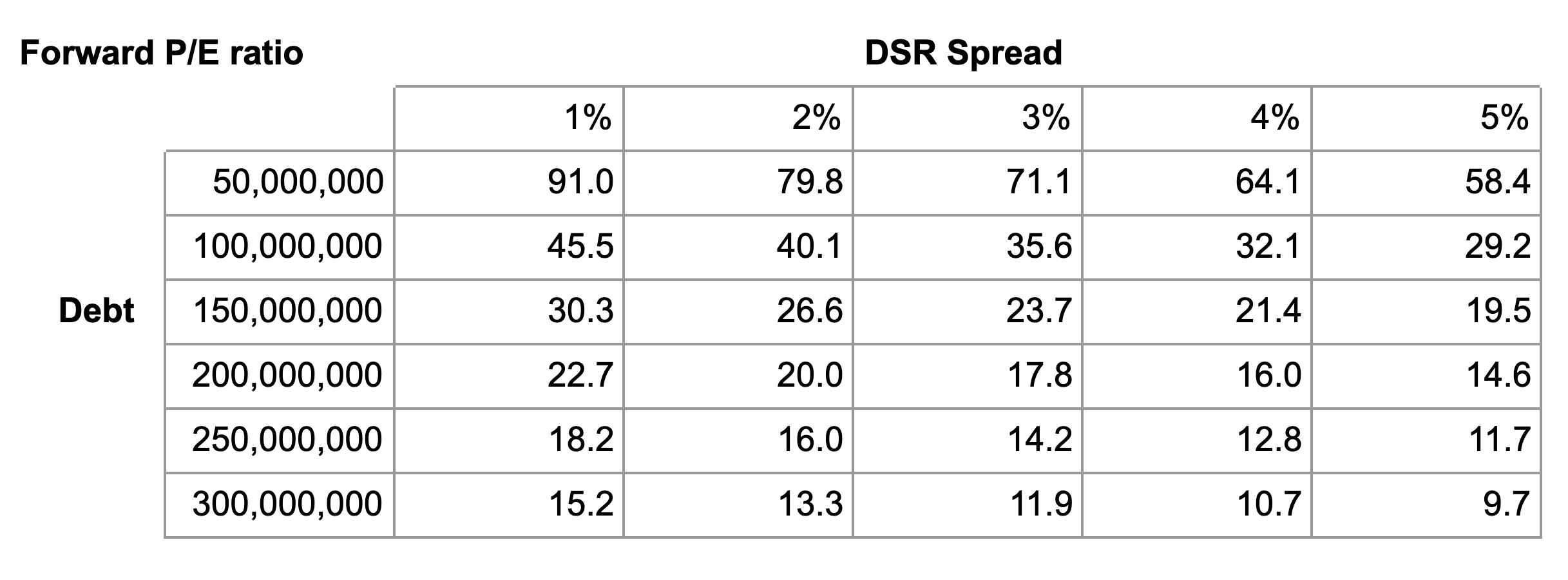

The average auction price of $243.9 implies a MKR market capitalization of $244.6m. In order to calculate at what forward P/E ratio auction participants recapitalized the system, assume some inputs for the next 365 days:

Stability Fee = 8%

DSR = 6% (DSR spread = 2%)

DSR utilization = 75%

Average DAI debt throughout the year = 100m

Bad debt = 0

No fees from SCD

Debt liquidated each month = 1.7% (based on 2019 comparable data)

100% of penalty fees successfully collected

Considering the inputs above, net revenue for Maker in one year amounts to $6.1m. This means that the forward P/E ratio at which MKR auction buyers made recapitalization measures 40.1. Sensitivity table on different debt and DSR spread inputs can be seen below.

Contributor: Lucas Campbell, Growth at DeFi Rate

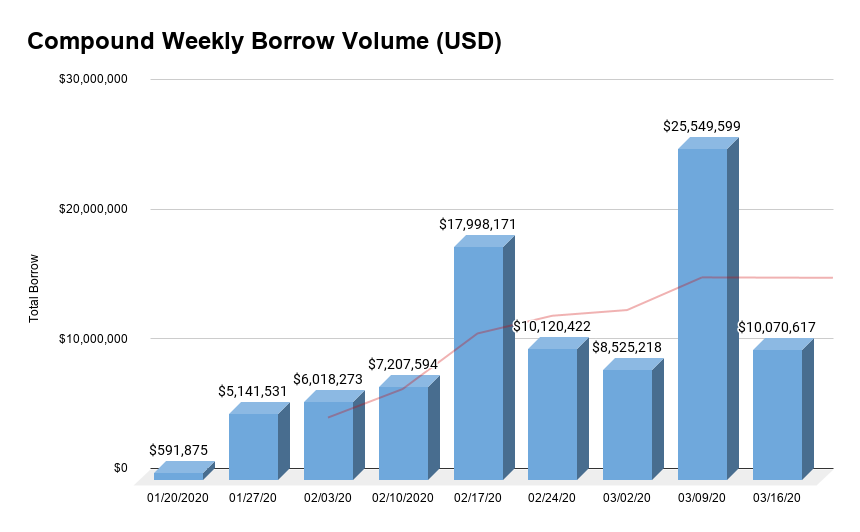

- Compound’s weekly borrowing volume has increased steadily since the beginning of the year. The lending protocol reached new yearly highs earlier this month after hitting $25.54M in borrowing activity across all supported assets. In March, the average weekly volume was $14.7M, up +42.37% from February’s average of $10.3M in loans originated.

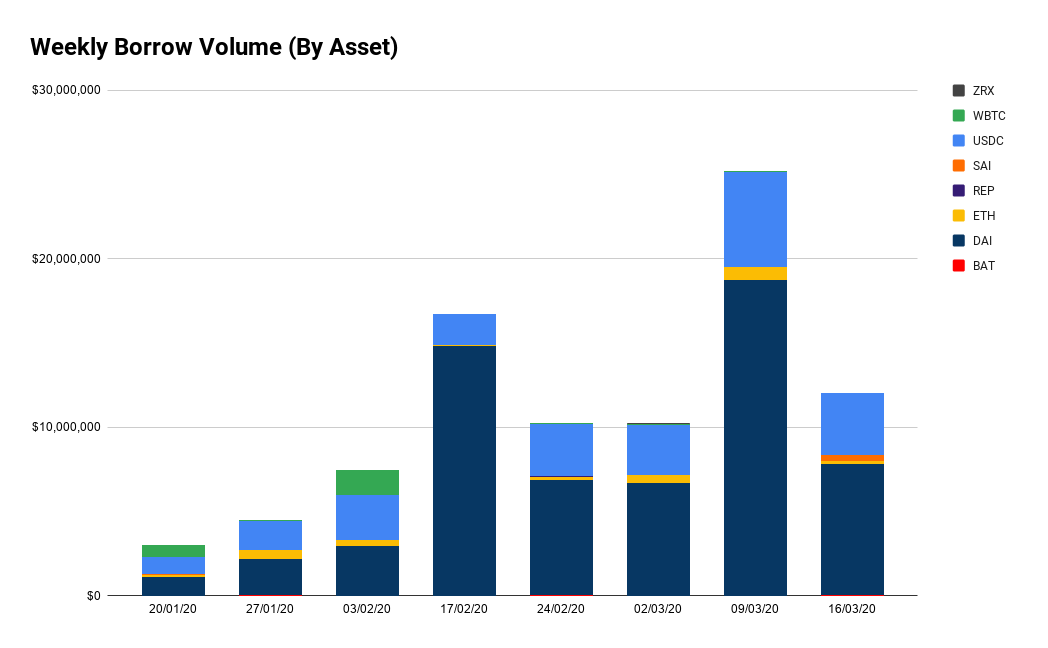

- Compound users are mostly taking out loans in either DAI or USDC - a common occurrence throughout lending markets as a whole. In the last 8 weeks, Dai borrowing volumes have substantially outpaced the rest of the field with over $61M in total volume. The second highest asset is USDC which only processed $22.56M in loans over the same time period. This is largely due to the two stablecoins offering the only attractive yields on the market. To highlight this briefly, Compound’s 30-day average lending rate for Dai is 7.66% while USDC’s sits at 2.27%. Comparatively, lending rates on other supported assets like ETH or ZRX are <0.02%.

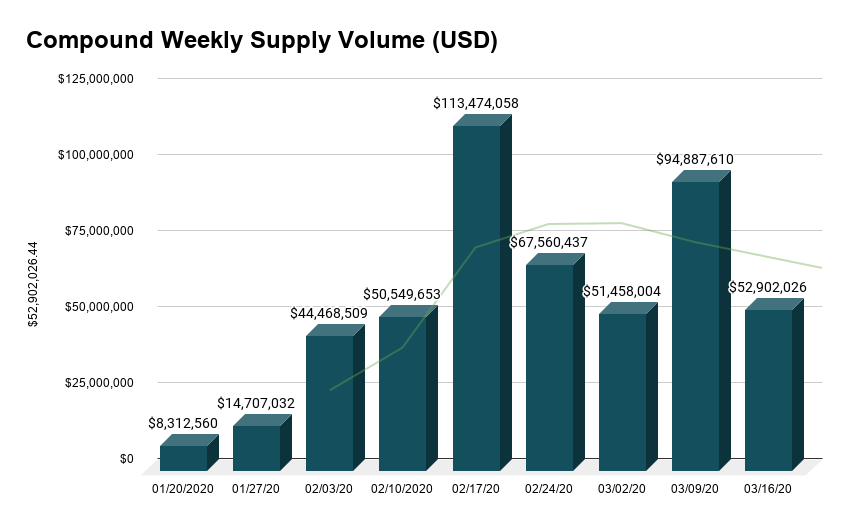

- Naturally with the rise in borrowing activity, there’s also been a moderate increase in Compound’s supply volume over the past 8 weeks. The protocol reached yearly highs of $113M in supply volume on the week of February 17th. The nine-figure record pushed February’s average weekly deposits to just over $69M, beating out March’s average of $66M by 4.34%.

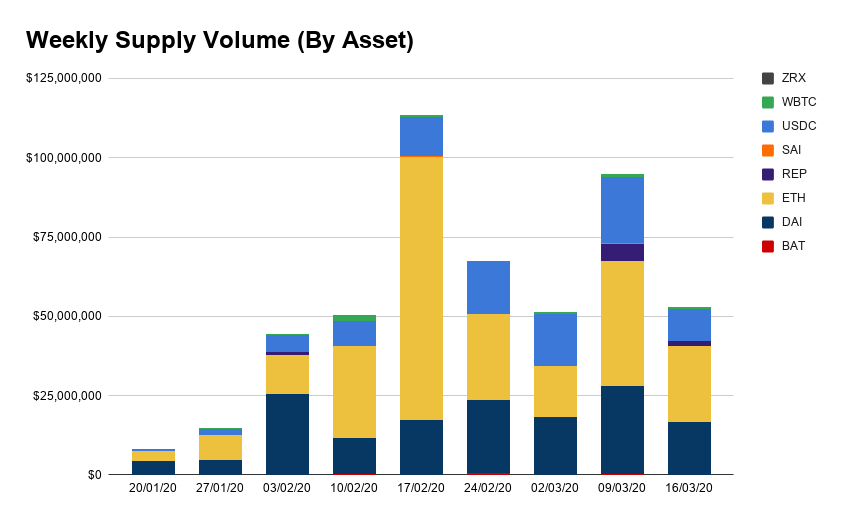

- There’s also been a surge in Ether deposits in recent weeks, making it the most liquid lending pool on Compound with over $41.61M in gross supply as of writing. The biggest spike was in February where the protocol saw $83M in ETH supplied to the lending pool in less than a week. With that, total ETH locked on Compound peaked at 517,000 ETH in early March as average weekly ETH supply volume reached $26.85M. Other assets with notable deposit volumes include DAI and USDC which have both remained relatively steady over the past few months. Since late January, DAI has averaged $16M in weekly supply volume while USDC averaged $10.2M.

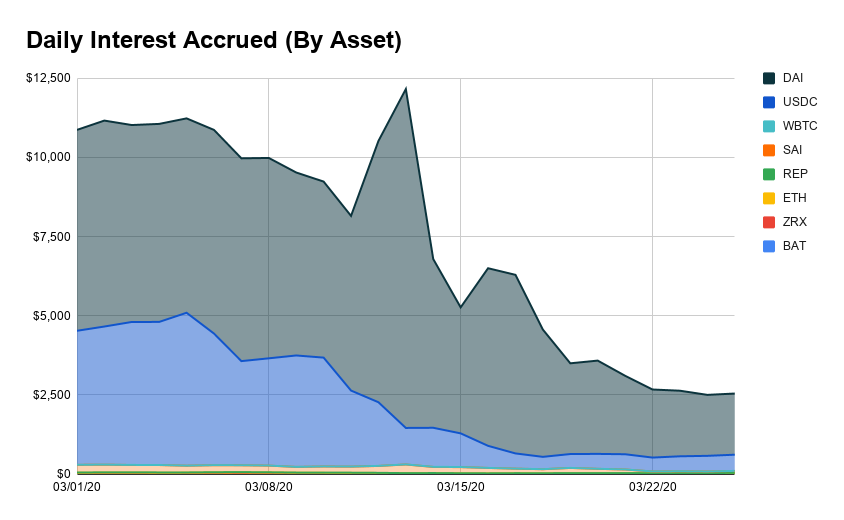

- While lending rates have fallen off due to Black Thursday and the DSR drop to 0%, USDC and DAI are the clear leaders as income-generating assets for its holders. DAI accounts for over 68% of total interest accrued this month on Compound, generating over $127,000 for cDAI holders. The other stablecoin, USDC, represents 28% of the protocol’s accrued interest in March, earning around $52,000 for cUSDC suppliers. The rest of the assets (BAT, ZRX, ETH, REP, SAI, and WBTC) account for less than 4% of the remaining interest with SAI having the most notable earnings out of the group with $4,323 in accrued interest.

Contributor: Isa Kivlighan, Aave team

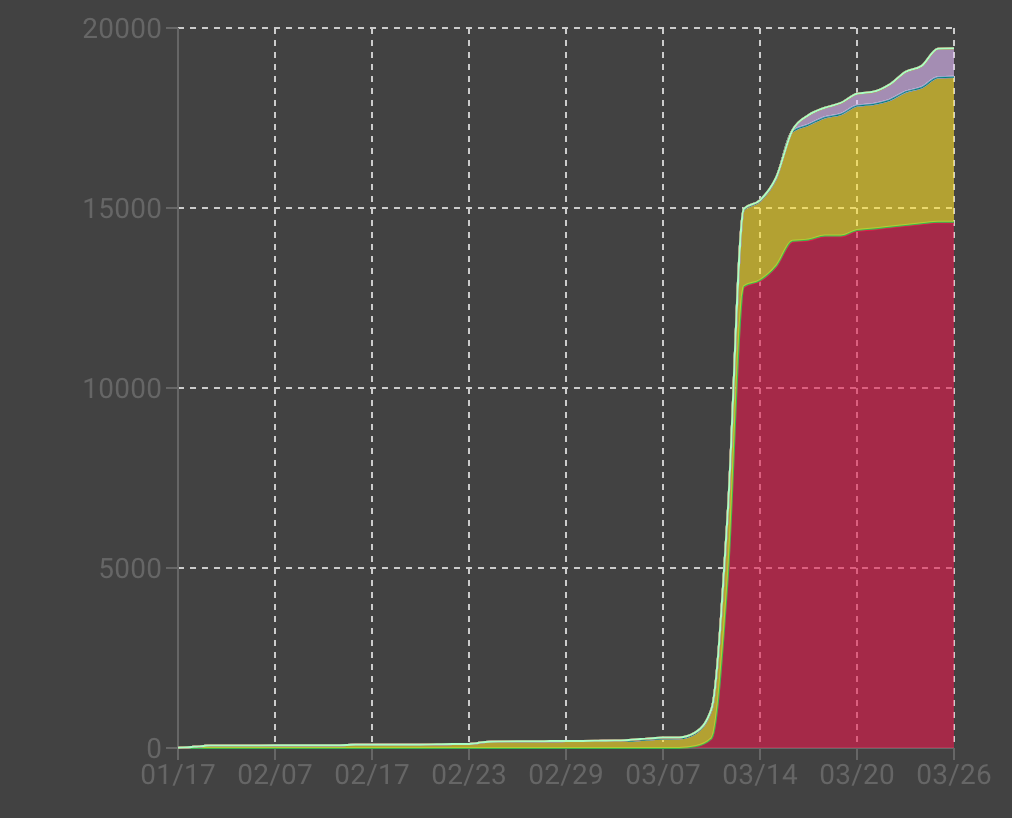

- Flash Loans Volume. Recently, one of the most interesting statistics is the huge increase in the volume of Flash Loans made on Aave Protocol the past 2 weeks. This spike occurred on 3/12, the day now known as Crypto Black Thursday. This increase was driven by the liquidations on Maker Dao. It is worth noting that DeFi Saver played a major role in driving up the Flash Loan volume on Aave on Crypto Black Thursday (source).

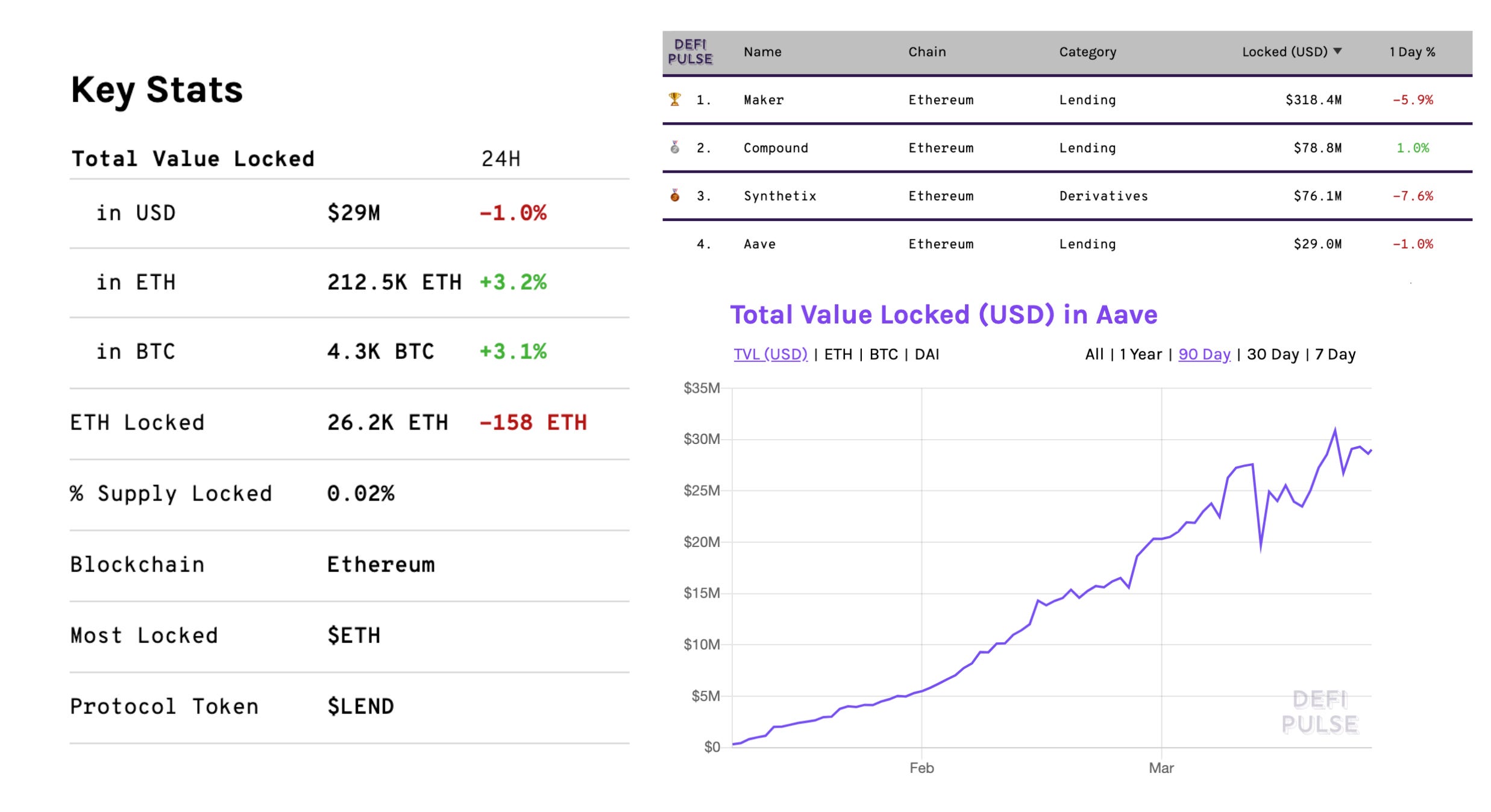

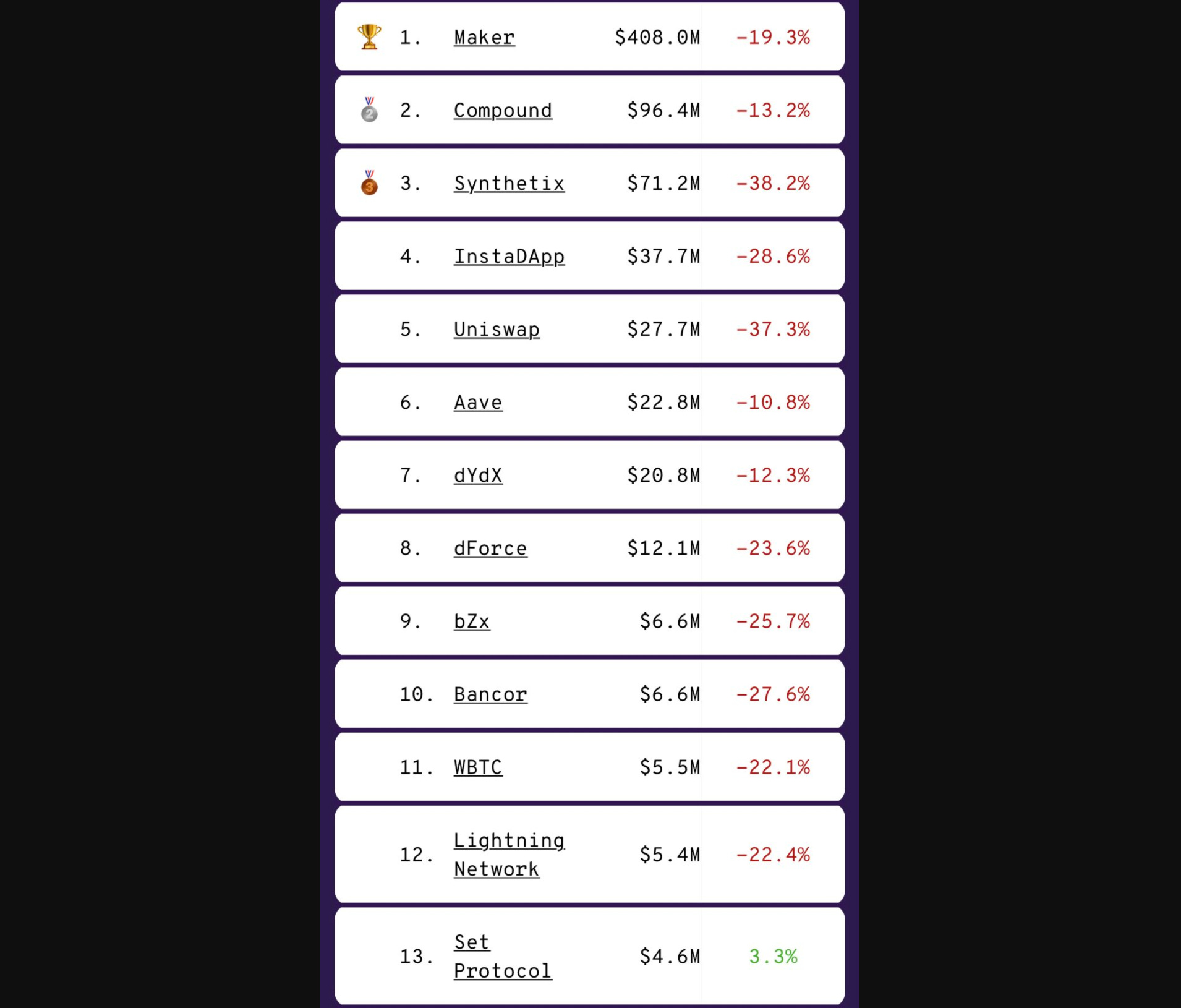

- After the Crypto Black Thursday liquidation events, Aave Protocol was not largely affected by the overall reduction in LTV. Aave passed from 5th to 4th on DeFi Pulse as a result.

- The market size of Aave Protocol has significantly increased (values are reflected in USD) recently. It now stands at $37.2M, with $29.9M total value locked and $7.3M total borrowed value currently (source).

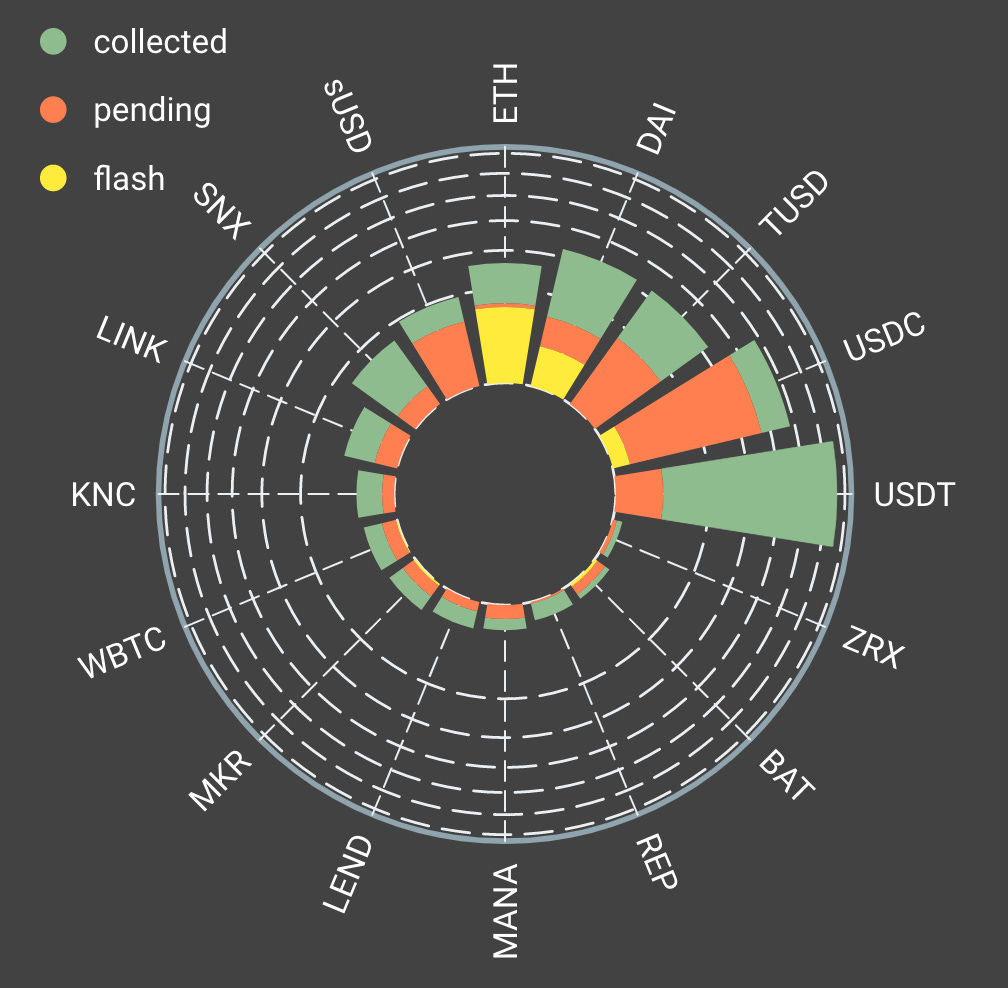

- According to Aave Watch, 266.76 ETH have been collected for protocol fees so far out of a total 363.23 ETH (the remaining pending fees will be collected in the future). Roughly 80% of fees go toward burning the LEND token.

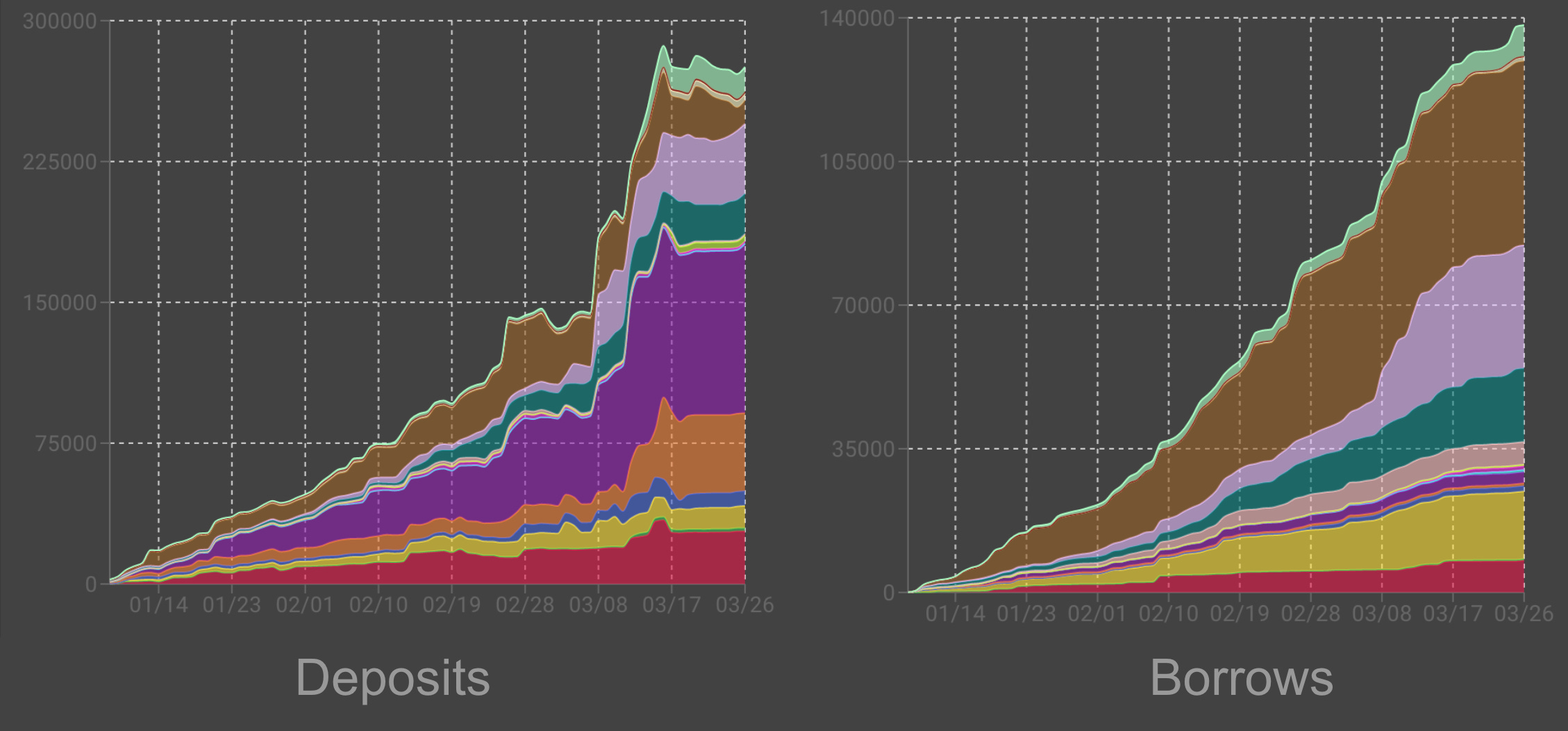

- Aave Watch shows that the volume of deposits and borrows (denominated in ETH) has steadily increased since the launch of Aave Protocol in January.

Contributor: Anthony Sassano, Head of Marketing at Set Protocol

- Over the last few weeks, Set has been working closely with imToken on exposing TokenSets to their users. Their team generously moved TokenSets to the Recommended Section of their app which resulted in imToken becoming a top 5 traffic source for TokenSets.

- Most Sets were positioned in USD during crypto's Black Thursday which resulted in Set Protocol's AUV being mostly unaffected and some Sets were even up 100%+ against ETH. The below image is from DeFi Pulse one day after Black Thursday.

- Set Protocol handled almost $3.4 million worth of buy, sell and rebalance volume on February 26th which was a new all time high for the protocol. This volume mainly came from rebalances with the largest being the ETH20SMACO Set ($1.2mil rebalance) and the yield version of the same Set ($842k rebalance).

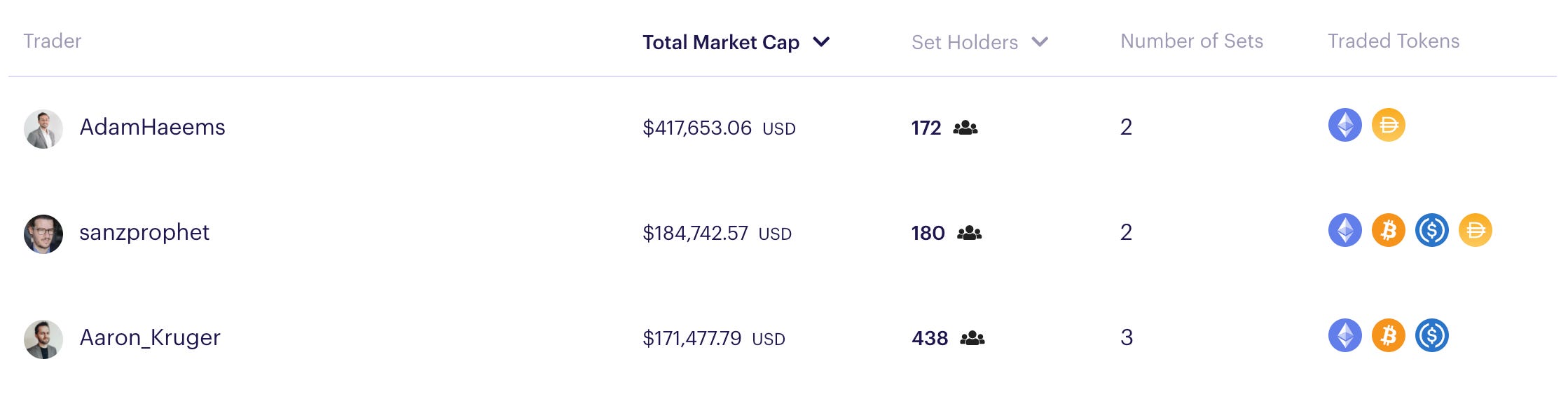

- Set Social Traders had a shakeup over the last month with Aaron Kruger falling from first to third in the rankings while Adam Haeems and Sanz Prophet rocketed to the first and second place respectively. This happened as a result of both of Adam's Sets being the 2 best performing social trading Sets since inception (up 83.8% and 65.5% against ETH respectively) and Sanz Prophets Set being the third most profitable Set as it's up 62.3% against ETH.

- Social Traders have accumulated over $24,000 in fees since we launched the platform a little over 2 months ago. It's important to keep in mind that these fees are just one time buy-in fees - we'll be deploying a more advanced fee structure very soon that'll allow traders to take fees based on performance.

About the editor: Spencer Noon leads investments for DTC Capital, a fundamentals-focused crypto fund. He actively tweets about on-chain metrics.