ON–062: DeFi

Coverage on MakerDAO, Curve, Terra, and Alpha Finance.

Mar 12, 2021

This is issue #62 of the on-chain analytics newsletter that reaches nearly 10k crypto investors every week 📈

About the editor: Spencer Noon 🕛 is an investor at Variant, a first-check crypto VC fund.

1inch, whose v2 offers the best rates by discovering the most efficient swapping routes across all DEXes—swap on the customizable new UI. And also Aave, where you can experience DeFi: Deposit, Earn, & Borrow on Aave.

This week our contributor analysts cover DeFi: Alpha Finance, Terra, Maker, and Curve.

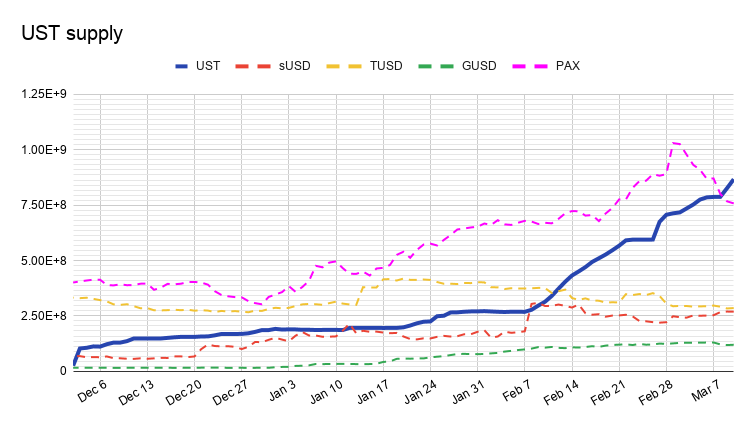

- Since the launch of Mirror in early December, Terra's overall stablecoin supply has increased by 2000%. The UST supply catapulted from a few thousand to almost 900 million in just 3.5 months, surpassing long-established stablecoins like Gemini Dollar, sUSD, TrueUSD, and Paxos along the way.

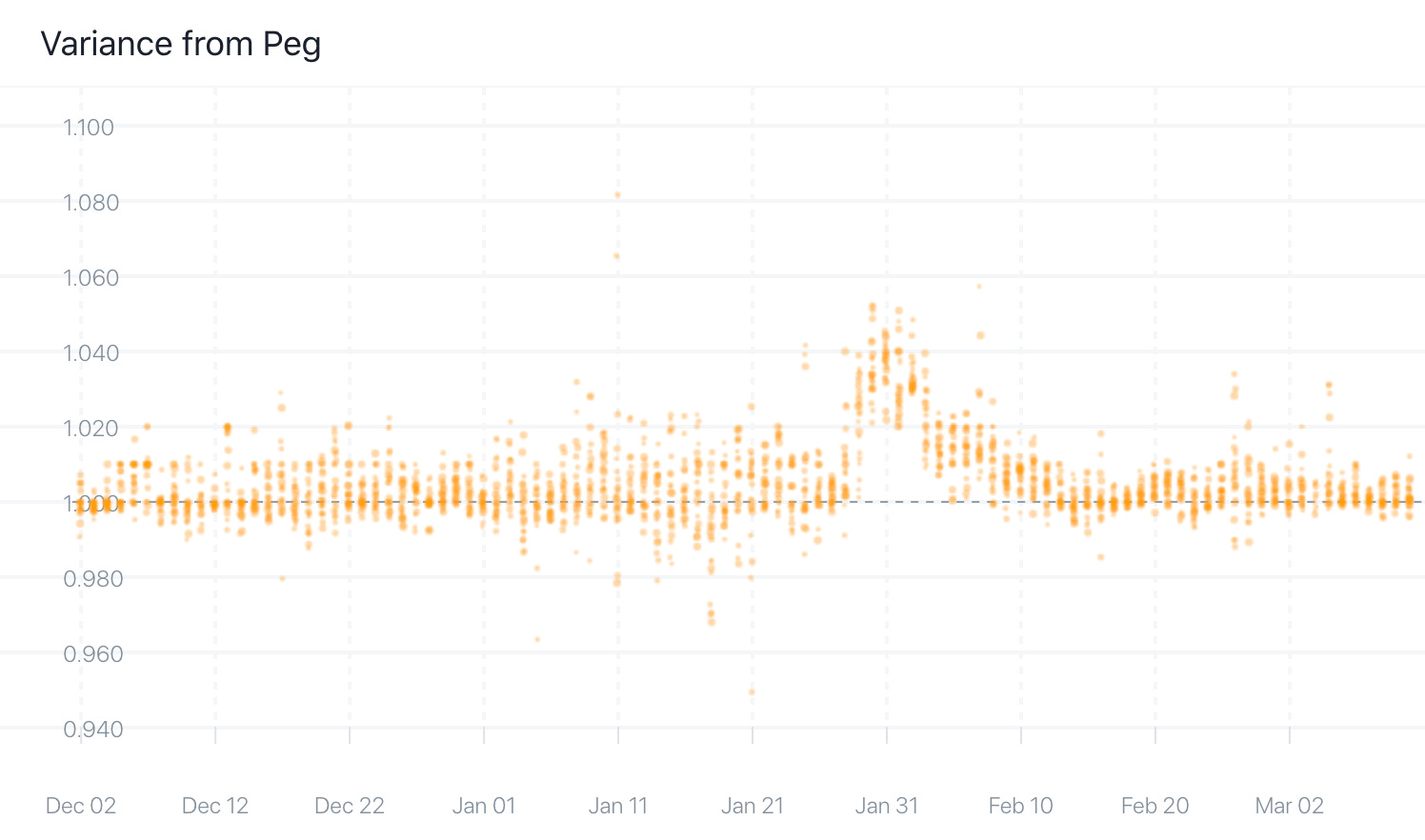

- With such a dramatic increase in supply, the peg of any stablecoin comes under enormous pressure. That said, aside from a few days in early February where UST was trading at up to a 4% premium, Terra's stability mechanism returned UST to the peg quickly and gracefully.

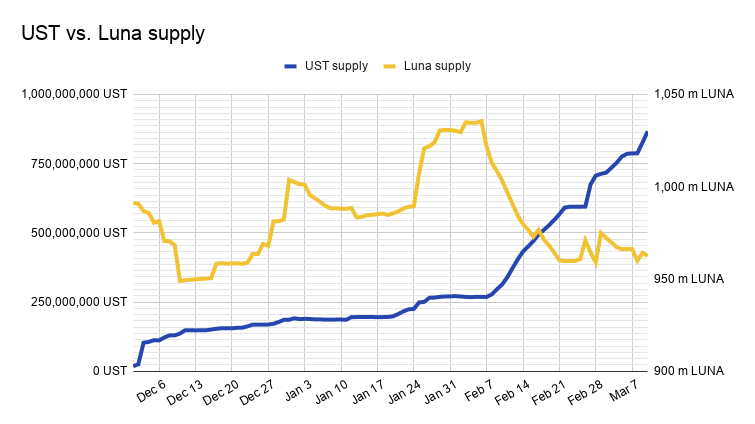

- Terra achieves stability by having LUNA absorb UST’s volatility. This means that it can be profitable for arbitrageurs to buy and burn LUNA to mint UST. Looking at the LUNA supply over the same time horizon as the UST supply increase shows that this mechanic has worked well so far.

👥 Tascha

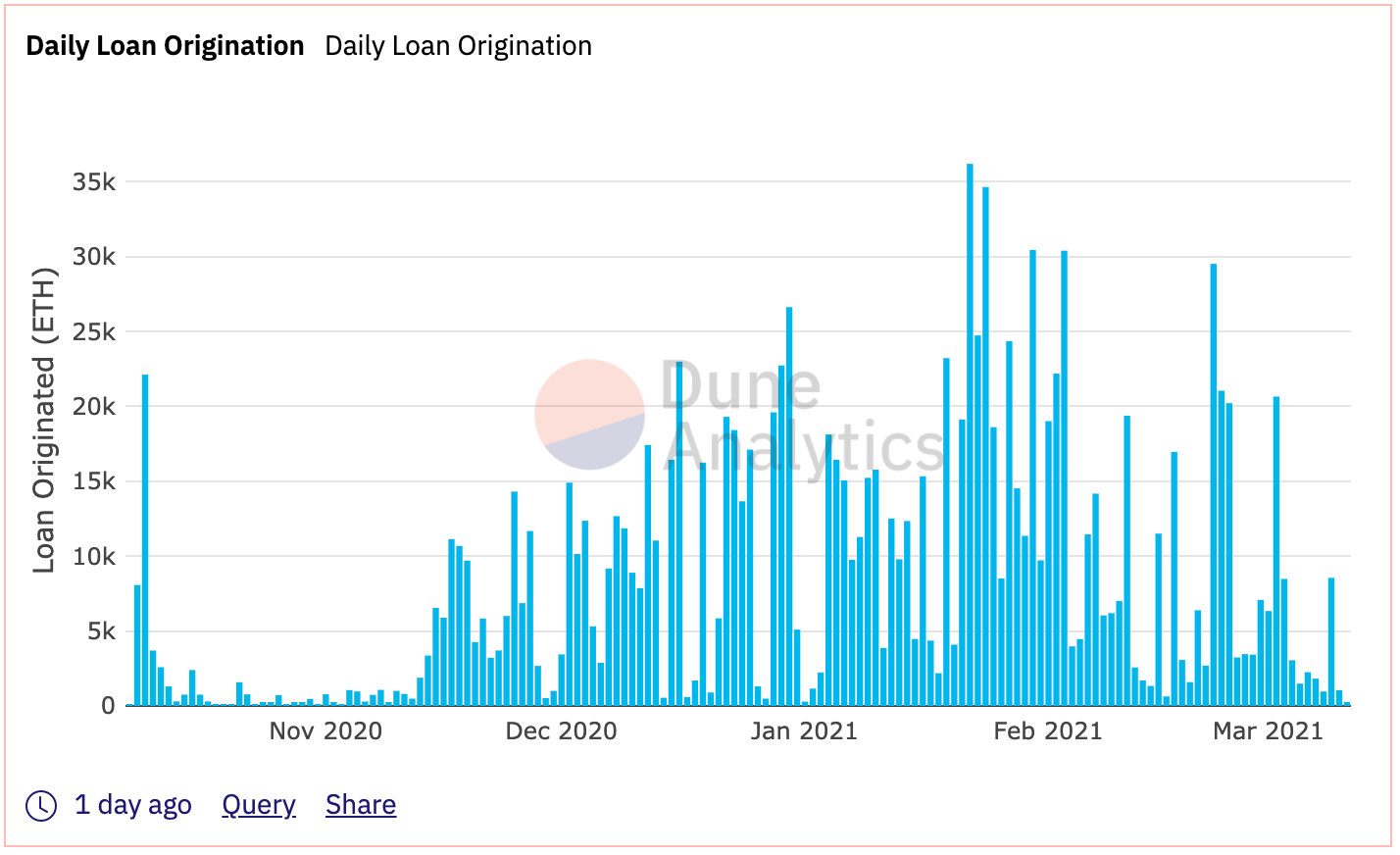

- Since launching in October 2020 (5 months ago), Alpha Homora has originated more than $2.29 Billion in loans (1.26M ETH). Loan origination is an important metric that correlates directly with the protocol fees collected, as fees are extracted based on borrow volume.

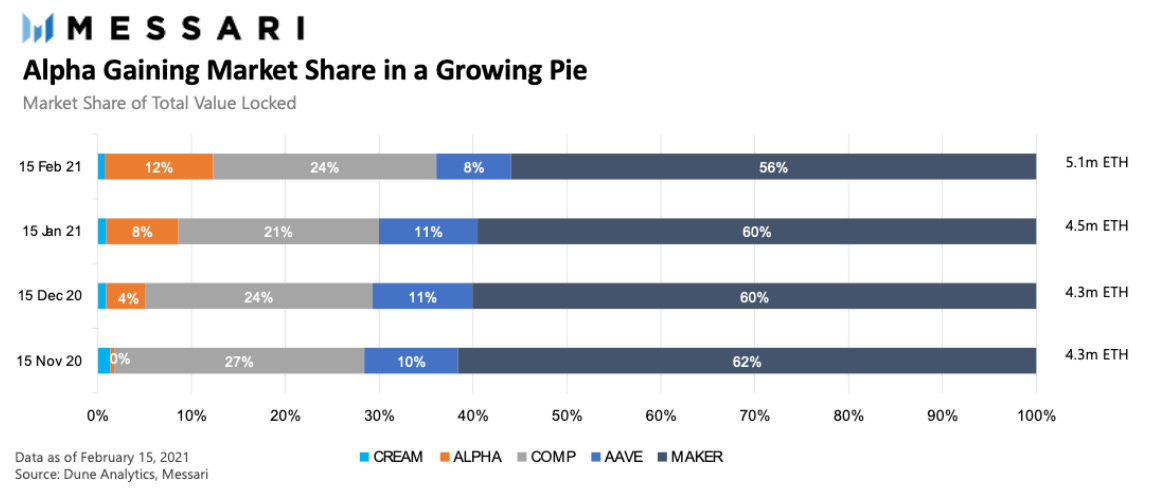

- In November 2020, Alpha Homora was responsible for just 0.5% of the lending market share based on TVL. In Dec 2020, it gained 4%. In Jan 2021, it gained 8%, and in Feb 2021, it gained 12%. While TVL is important, TVL retention is crucial to understand product-market fit and the value the product brings to the market.

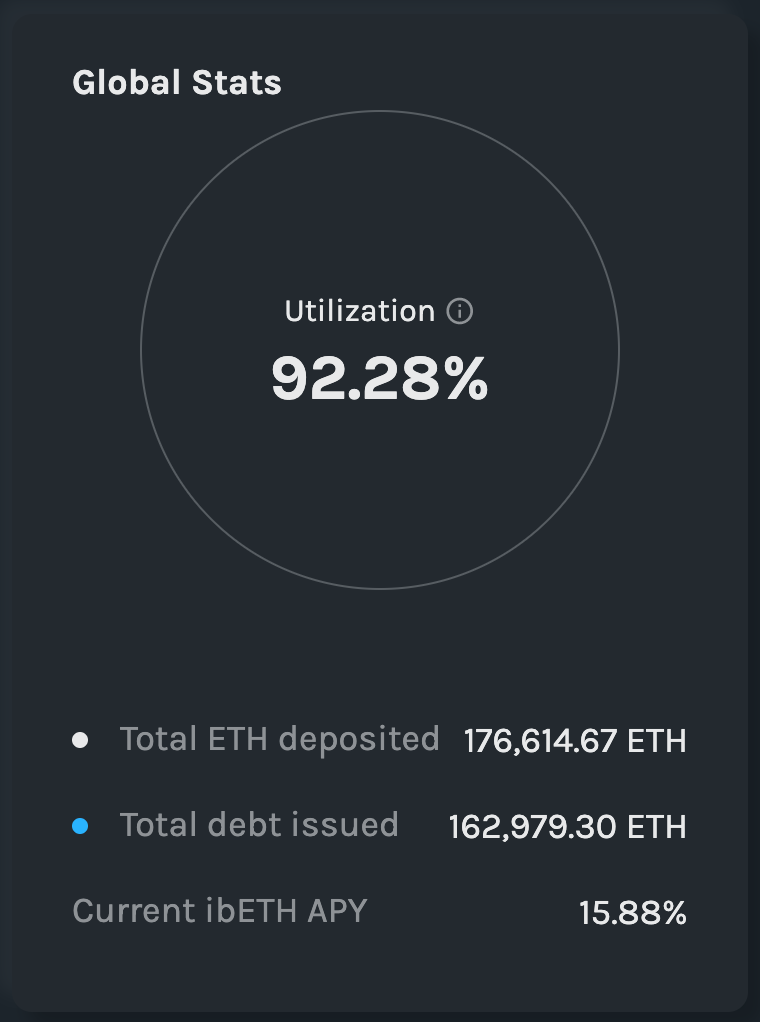

- The ETH utilization rate on Alpha Homora is usually around 80-95% and the typical yield on ETH on Alpha Homora is 7-10%. Many protocols can attract supply through incentives, but utilization (% of the assets supplied that are borrowed) shows how sustainable it is to generate high yields to lenders.

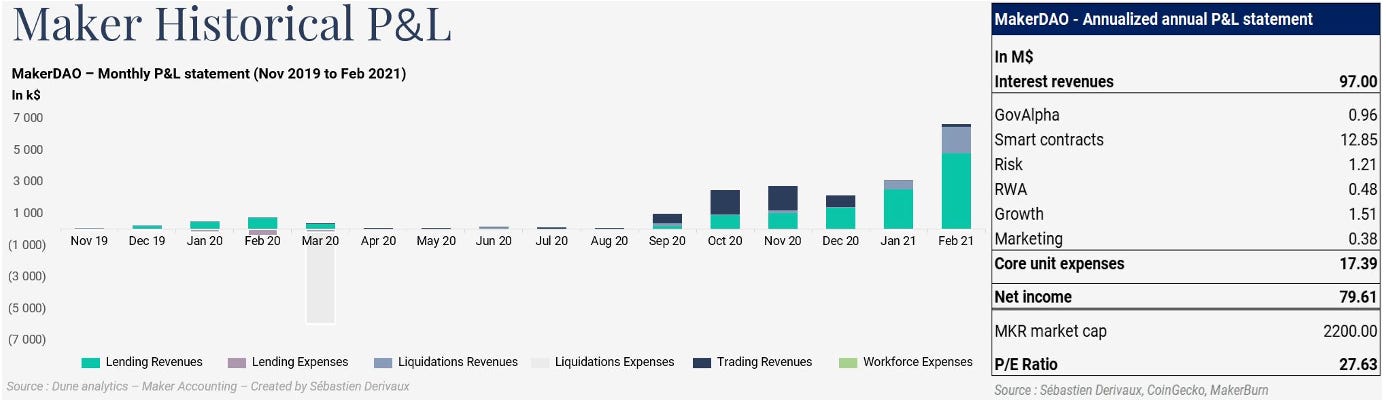

- MKR monthly net income increased 1700% YoY to $6.6M. Based on current run rates, this implies an annualized net income of ~$80M ($97M-$17M core unit expenses) for a current P/E ~28. (Note: this figure excludes net PSM revenues, net liquidation revenues & assumes no growth.)

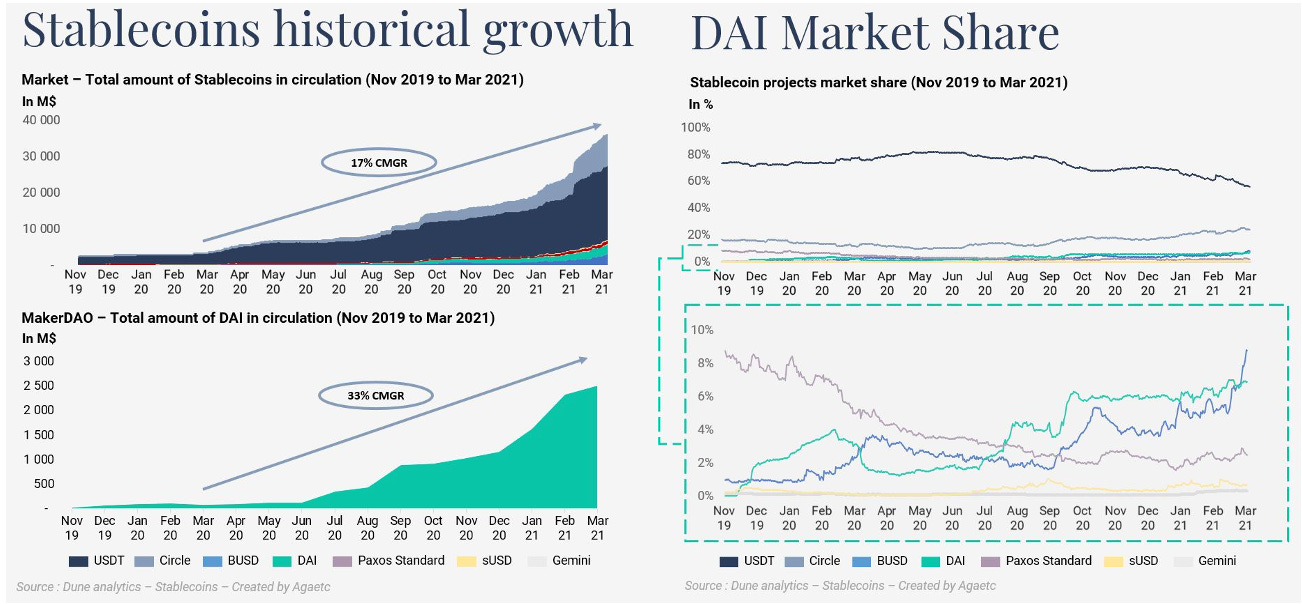

- DAI is increasing its market share in the growing stablecoin market. DAI supply has increased at a compound monthly growth rate (CMGR) of 33% over the last twelve months, while the overall stablecoin market increased at a CMGR of 17%. Over that period, DAI market share increased from 3% to 7%.

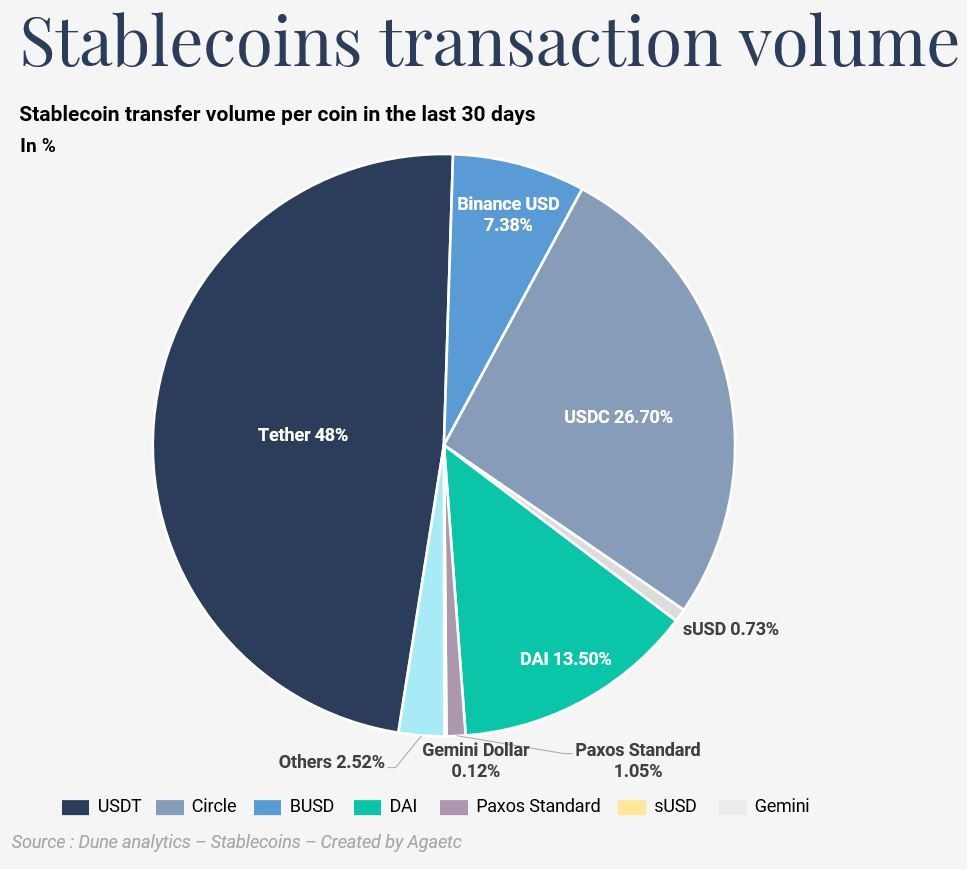

- Finally, although DAI represents only 7% of the overall stablecoin market, it accounted for 13.5% of all transfer volume in the past 30 days. DAI also has the highest velocity of all stablecoins, in part due to its smaller size.

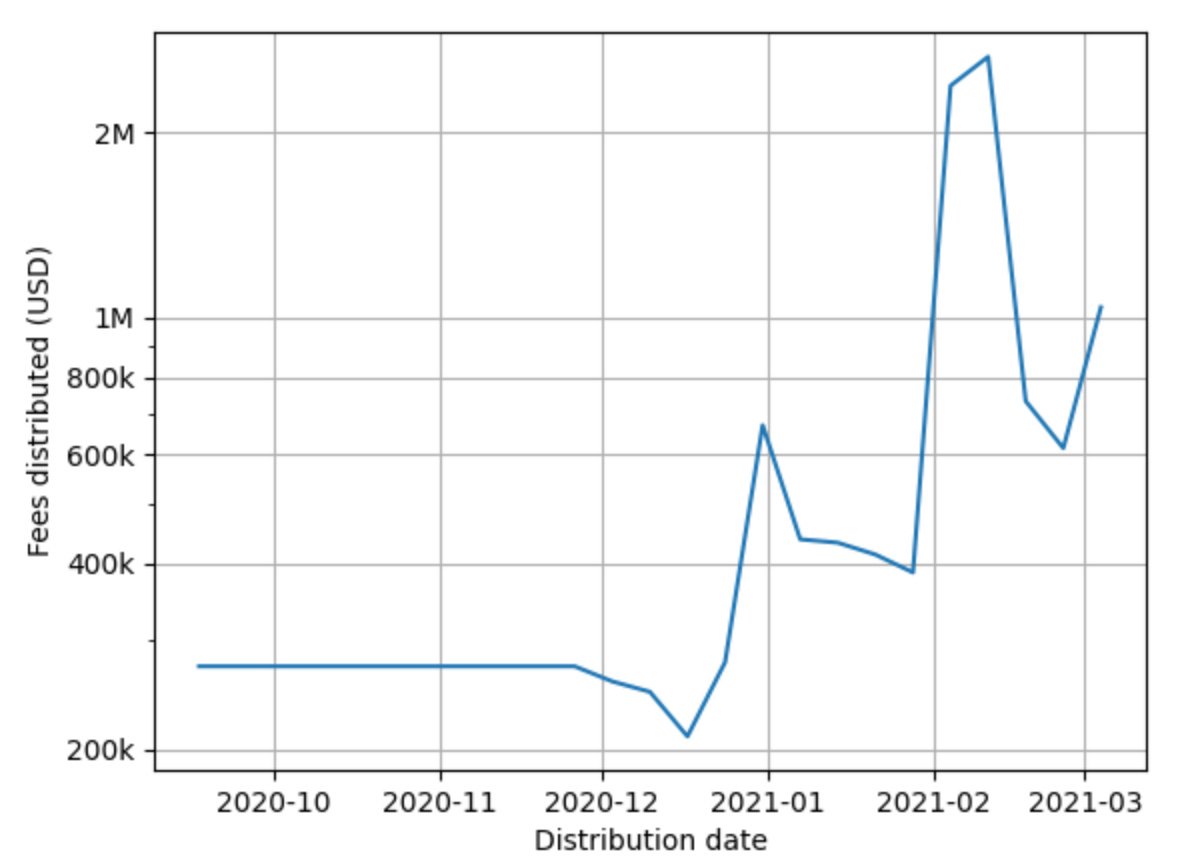

- Curve DAO forwards 50% of all fees charged for swaps to participants in governance who lock CRV. The weekly amount of those fees grew up 3x in 3 months (on average).

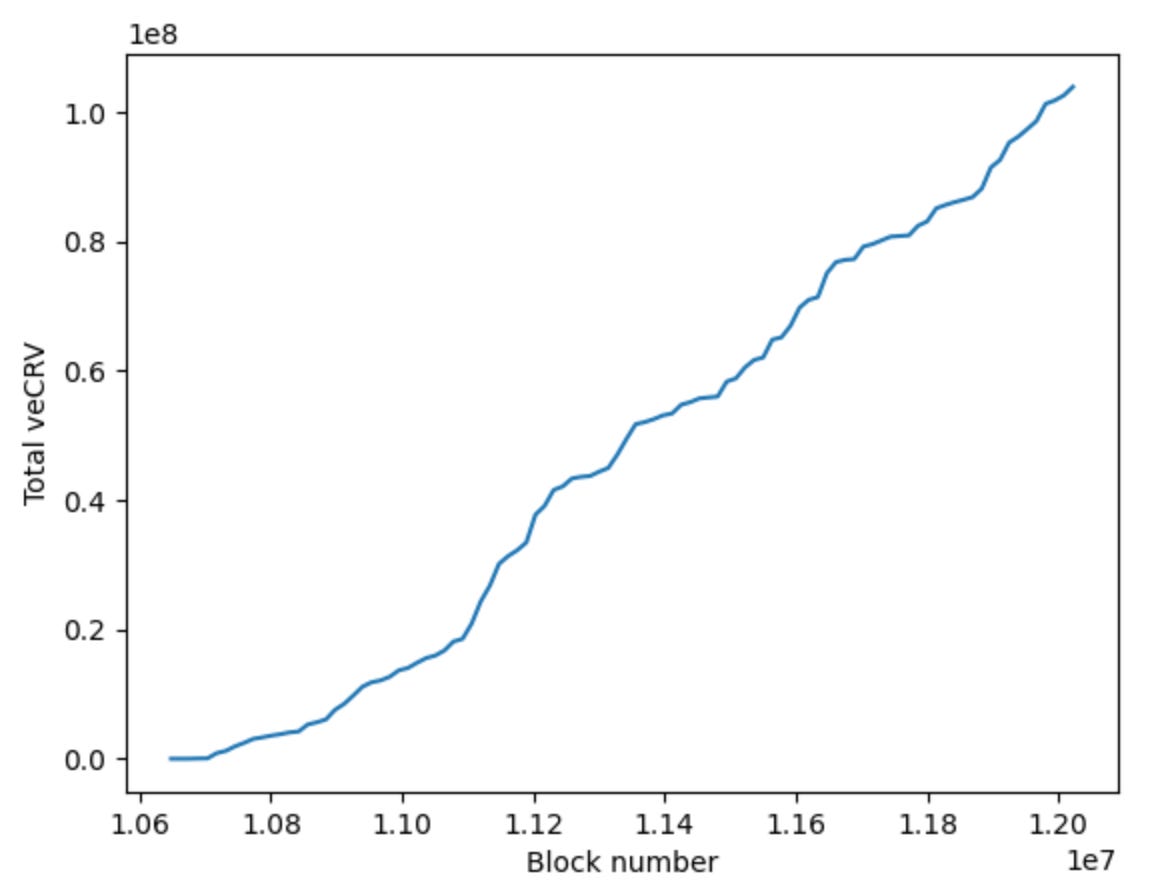

- The amount of CRV locked for governance (to be able to vote and receive the mentioned above admin fees) now exceeds 100 million CRV (~$200M).

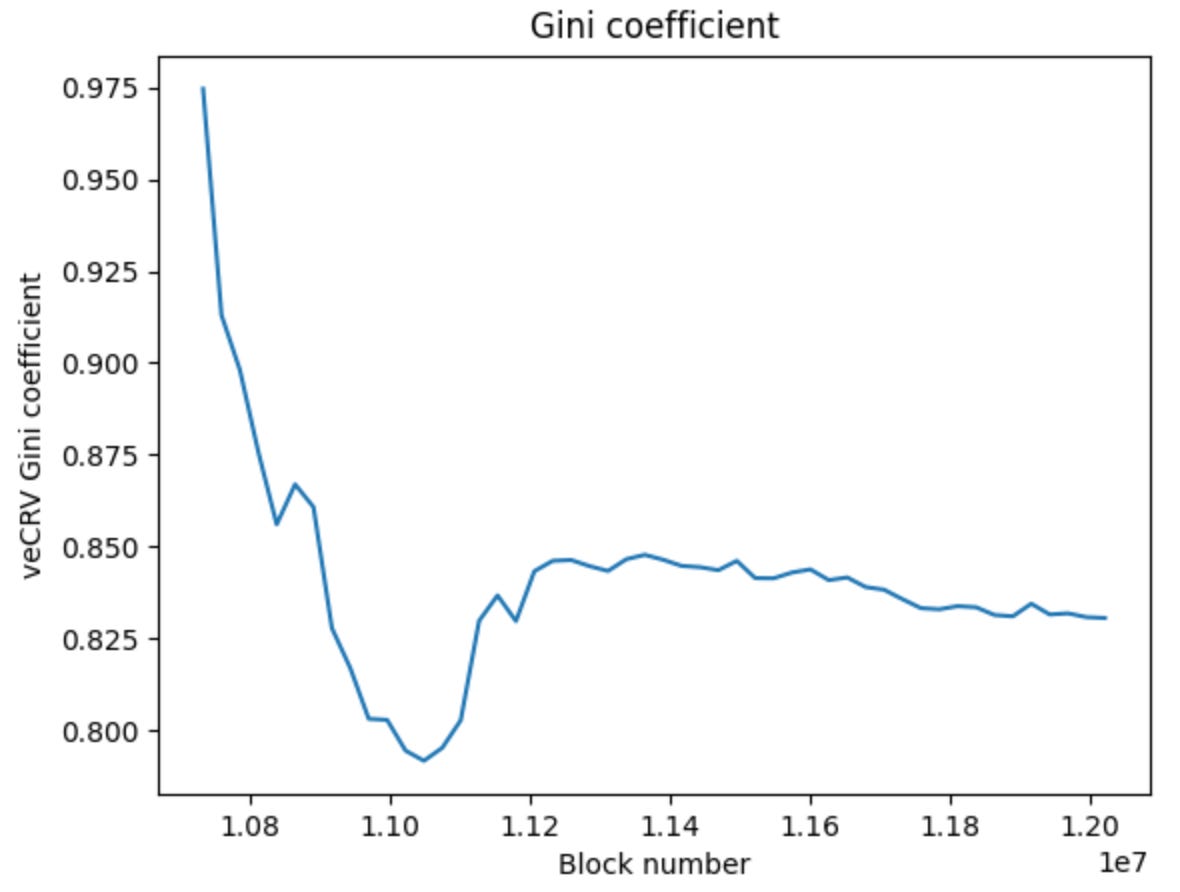

- Gini coefficient is used to measure the decentralization of voting power. For Curve, the coefficient is hovering around 0.83.